By Tom Luongo

February 1, 2023

With the markets still firmly convinced the Federal Reserve will hike the Fed Funds Rate by just 25 basis points (0.25%) on Wednesday, I find it fascinating that no less a figure than Mohamed El-Erian, former head of PIMCO, argued for the Fed to stay the course and surprise markets with another 50 basis point move this week.

I agree with him. Completely.

I know you're shocked.

This article came out on the same day as the latest US GDP figure (Q4 +2.6%), home sales (slowing but not terminal), inventories (down), and jobless claims (uninteresting). It was followed up with week ending data about consumer spending and the Fed's favorite inflation indicator, the PCE deflator, coming in cooling as expected, and now just barely below the FFR, 4.4% vs. 4.5%.

Oooh, positive real yield expectation of 0.1%. Quick, everyone the Fed made it safe to save in dollars again!

As the kids say on teh Twitterz, "SMFH."

El-Erian made a number of points that support the 'normie' interpretation of Fed policy about taming inflation. They are good ones if you believe inflation is the Fed's top priority (and not one of many priorities):

- While inflation will indeed continue to come down in the immediate future, its main drivers have been shifting to the service sector, thereby increasing the risk of more embedded price pressures when the labor market remains solid.

- With global growth surprising on the upside, the window for more orderly rate increases has been opened wider.

- Financial conditions have loosened significantly in recent months and, by some measures, are around levels that prevailed last March when the Fed initiated this hiking cycle.

- A faster journey to the peak rate that has already been signaled, and reiterated by Fed officials several times, reduces the complexities of linking the path to a variable destination.

There are also strong risk-management arguments in favor of another 50-point increase before downshifting to 25 basis points.

I like El-Erian's second and third points best because they support the argument that I made in this month's lead article in the Gold Goats 'n Guns Newsletter that "There Is No Recession" coming in 2023.

Most likely 2024, but very unlikely 2023.

Global growth is not likely to go negative with these tailwinds:

- A mild winter in Europe implying lower energy costs for Europe this summer

- A counter-trend rally in the euro feeding directly into that 'lower energy cost' than forecasted for Europe thanks to higher FX bias.

- China ending its Zero-COVID policy to coincide with Janet Yellen's Russian oil price cap implying China comes out of the COVID lockdown period ready to explode, esp. with a yuan below ¥6.8 and the PBoC having room to 'expand.'

- Yellen doing a variation on Operation Twist to counteract Powell's QT and spending down the Treasury's GA balance.

- Last year's blowout $1.2 trillion in new credit creation domestically fueling all manner of spending.

- Increased defense spending by the "Biden" administration.

- A tight labor market that will continue to rotate out of human resources masquerading as tech jobs and back into moving things around.

All of this data prompted the folks at Zerohedge to engage in a bit of projection saying that Powell is perplexed by the labor data.

This is not the picture that Powell is hoping for given the unprecedented tightening of monetary policy he has unleashed over the last year. There is nothing in this data that warrants a 'pause' by The Fed.

Yes, Tylers, you are correct the Fed doesn't need to pause.

And no, Tylers, you are the ones perplexed because your basic premise continues to be wrong. The Fed can't really fight this inflation because it's not a credit demand inflation, which is what interest rates have the most control over, and short-term rates only then.

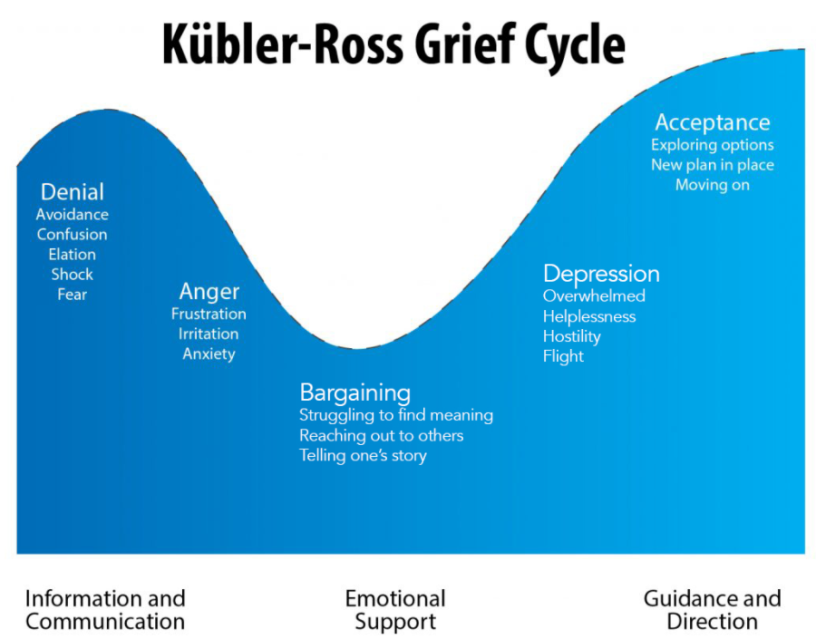

This data just gives FOMC Chair Jerome Powell more ammo to do what El-Erian and I are urging him to do, raise by 50 bps and move another tranche of investors out of 'bargaining' and into 'depression' on their way to 'acceptance' that the Fed Put is dead.

From where I sit the markets have finally moved on from 'denial' (for the most part) and are into 'anger.'

The reality is that they should be getting closer to 'acceptance' that there is something else going on here than just the Fed trying to tame inflation.

There was a marked shift in market sentiment after Thursday's GDP data. Treasury yields started rising, gold stopped dead and stocks didn't do much of anything. This is not the confident picture of a dovish Fed on Wednesday.

Friday's inflation data was also non-confirmatory of the need to slow things down. What bothers me most about all of this is that for so long the Fed caught flak for not raising rates and then when they finally do, it's all this "but they'll just pivot at the first sign of trouble," nonsense that's been the refrain since the first 25 bps rise last March.

The first signs of trouble are already here: car loan delinquencies, housing slow downs, credit card usage rising, car prices falling alongside corporate earnings necessitating big announced layoffs in tech. So, the Fed has withstood much more than it did under Bernanke and Yellen.

And yet the pivot talk is still all the rage.

Right Or Honest... Choose One

You know, every time I'm confronted with a situation like this I'm reminded of my very first phone call with Newsmax where they were interviewing me to take over one of their financial newsletters.

The person who would become my line editor and teach me how to write one of these things, very pointedly asked me, "Would you rather be right or honest?"

The implication being, you are going to be wrong from time to time, can you handle admitting it publicly and accepting responsibility for it? I guess I answered correctly, because I got the job. But I wasn't lying. If I'm wrong, I'm wrong. I'll own it.

Today, if I'm wrong about Powell and he only goes 25, I'll take the hit.

Too much of what I see in financial commentary today is good people who cannot admit that they may have gotten this cycle from the Fed wrong. They are scared for their reputation and for their business.

Hey, I get it. Do you think I don't feel that everyday? We all do. This is a tough business hanging your ass out over a cliff with imperfect, if not purposefully manipulated, data and making bold calls.

I applaud anyone even trying it.

But, that said, being wrong for years until you are right isn't a virtue. Doing your best impression of a stopped clock is dishonest.

So, to my alt-finance brethren: Do you want to continue 'talking your book' into a kind of Fed-mageddon rather than accept a different thesis and wind up a meme like Jim Cramer?

My point is ultimately, that folks like the Tyler who wrote that piece above spend so much time begging their own question they never spend a minute wondering if there is a different or better question they should be asking.

Not My Eurodollars, Not My Circus

Which brings me to Jeff Snider and all things Eurodollars. Snider is the guy who popularized the Eurodollar analysis of the Fed's monetary policy. And we owe him a debt of thanks. I know I do.

The problem, as I've pointed out previously, is that Snider isn't a geopolitical guy. At best, he doesn't see the bigger picture of why the Fed would even be willing to try and break the Eurodollar market's hold on Fed policy.

At worst, he's potentially a shill for Davos, because he's argued the Eurodollar system is the free market response to the Fed's central planning. The truth is likely something else I haven't considered.

His latest rant (linked below) is that it's impossible to break the Eurodollar system.

This is good, it means my arguments are forcing people to react and steel man their positions.

Regardless of the why, Snider keeps doubling down on his view that the Fed is both incompetent and evil. Stop me if you've heard this basic argument before.

There is zero willingness to engage in anything close to a reframe of the situation. Only the same auto-pilot analysis that's been, frankly, consistently wrong for now two years.

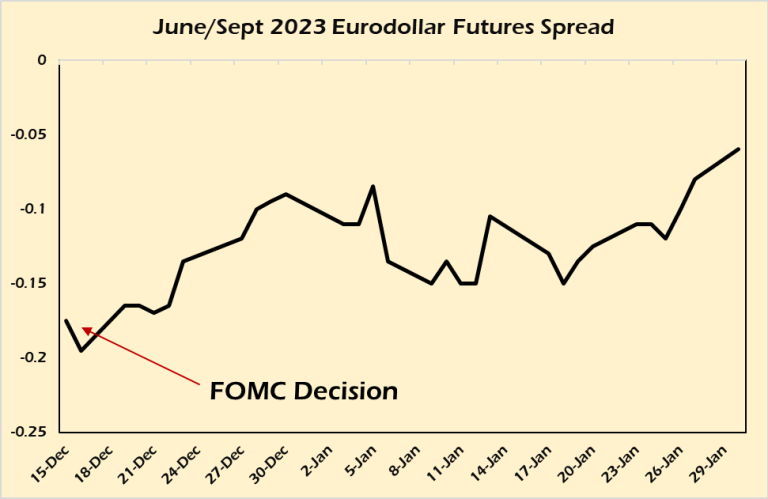

Snider wasn't wrong about the Eurodollar markets when Bernanke and Yellen were at the Fed. He was correct and a very valuable voice in the space. I listened very carefully. Eurodollar futures inversions always meant the global economy would seize up at the point of the inversion.

And today Eurodollar futures inversion is centered on June 2023. But last year it was centered on Q3/Q4 of 2022. So, is it right or wrong? Clearly in early 2022 the Eurodollar futures market was mispriced. Could it be mispriced for Q2/Q3 of this year where it's signaling the Fed pivot?

It's a good question.

At this point the Fed pivot has more in common with Schroedinger's Cat than it does with even Punxsutawney Phil.

But did those "Eurodollar events," as Snider calls them, occur because of the power of the Eurodollar markets (which now Snider says aren't even dollars anymore, just credit claims to dollars) or because Bernanke and Yellen are tied to the globalist cabal that built the Eurodollar system in the first place during the rebuilding of Europe under the Marshall Plan?

This "Shadow Banking" system became the tail wagging the Fed's dog. It was only because of entrenched market structures that supported and perpetuated this perceived power. In other words, was Snider's Eurodollar thesis built on an independent or dependent variable. And all he's done is rightly described market conditions of a past that no longer exists today?

Because of this inherent bias in the data (one where Eurodollars are supported by LIBOR and a willing Congress/FOMC) it has trained a whole lot of investors to analyze markets based on that assumption and believing it is a FACT incapable of change.

I'm just the guy with a can of coins trying to get everyone's attention and consider the following:

Anything that threatens the Eurodollar system is to be stamped out and the use of Eurodollar futures to manipulate global finance using a compliant Fed must be preserved at all costs.

I believe the latter thanks to the actions of Powell and John Williams at the New York Fed and their ending the use of LIBOR as the US dollar's primary debt indexing rate. This is the frame all of my arguments with respect to the Fed's main policy objectives this cycle.

This argument reduces to the use of Eurodollars to fund the US empire and the European Union while Europe retains control over 'their money' is the real story.

Snider, to repeat, is on record saying it's a 'free market' solution to the evil of the Fed.

Really? LIBOR, a free market. Again, as the kids say, "Ok, Boomer."

I leave it to you to decide who's frame of what Eurodollars represent is more accurate. And for the record, I'm not bitter or angry. I'm an asshole, and like Powell, I have "resting hawk face," so I can understand the confusion.

One of us will be 'right.' But the goal isn't about chest-thumping, it's finding the truth.

Because only with something close to it can we make good decisions with our money and time.

Future Considerations

Now, back to the core Eurodollar problem the Fed is facing.

Today the ED futures inversion is centered around June and a 5% pivot point.

What else ends in June? USD LIBOR usage for all US originated debt. Hmmm, convenient that. A major Canadian Bank, TD North, by the way, just joined the SOFR train for USD debt. So, that market's only going to get deeper and more liquid.

Clearly there is a bet being laid into the credit markets that the end of LIBOR will mark a turning point in Fed policy. And at that point, if you defer to Snider's analysis, the Eurodollar system will bitchslap the uppity Fed for thinking it had any real control over US monetary policy.

Now, let's think about this for a minute. Why are the Eurodollar markets obsessed with 5% as the 'pivot' point for the Fed?

I don't have an answer for that directly. But, let's make an assumption that something vital in Europe breaks if the FFR goes significantly above 5%. Would you not expect to see the histrionics we've seen from the financial press who we know for a near fact work for Davos?

Therefore, those histrionics can be seen as prima facie evidence that there's a need to keep the Fed below 5%. The massive overstatement of the economic data just feeds the beast that the Fed has already broken the world and it needs to stop before it breaks anything else.

But we know that's not the case. The data is nowhere near that bad.

For pity's sake, the Fed hasn't even given us one quarter of positive real yields on 2 year debt to make up for the past fifteen years of balance sheet erosion for nearly everyone except the Cantillionaire classes doing most of the complaining.

I don't know about you folks but I looked at my normal savings account at my primary bank and guess what my return is on that account?

4%? 3%? 2%?

No. It's still 0.015%

If you want a decent return on your money you have to tie it up for 9 to 24 months, still. And, by the way, if the punditocracy is correct and inflation comes down further (a bad assumption) then over that time even a 3% APR 12-month CD will still lose purchasing power.

The Fed isn't close to being done here and El-Erian is right that there is still a massive credibility gap.

Danielle Dimartino Booth noted this in her interview talking points during the second half of 2022, saying that Powell was angry at his staff for misleading him on inflation and leaving him out to hang with that 'inflation is transitory' bullshit in 2021.

The 'inflation is transitory' talk from the Fed was simply an outgrowth of the unprecedented political attack on the its leadership, led by none other than Lael Brainard, who was groomed by Obama to be Powell's replacement.

Still think there isn't a geopolitical angle to Fed policy? If you do you just might be Jim Cramer.

Consensus This!

So, while everything is screaming the Fed is going 25 bps this week there are very powerful arguments that have little to do with 'data' and more to do with 'the big picture' which says the FOMC is going to surprise us.

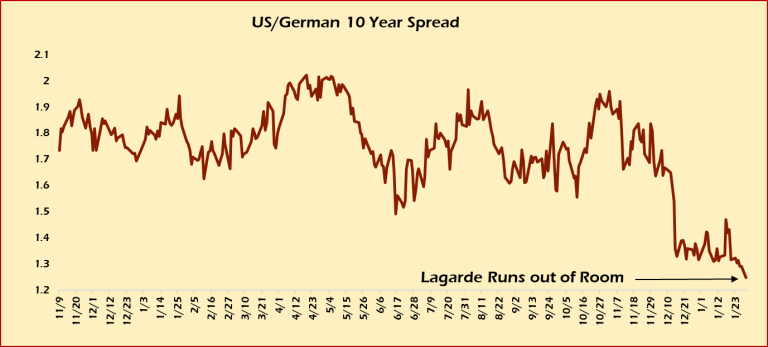

I'm sure you are getting tired of seeing this chart from me but this is the chart that matters. If the Fed is only going 25 bps and the ECB going 50 wouldn't we have seen a bigger shift here like in December?

With Euro-zone inflation far hotter than the US why does the market continue to disbelieve Powell, who has been straight with the markets for a year, while accepting that Lagarde has everything well in hand even though she keeps pivoting all over the place?

Here's the better question in response to a very good article at Wolf Street:

Wolf's got some good questions about that. When everyone was levering up ZIRP bucks, don't fight them. When the Fed says, "we're serious, no more ZIRP bucks."

Everyone's like "fight me, bro!"

The point of this chart is to show that Lagarde is losing the trust of the markets, she's moved heaven and earth to maintain internal credit spreads and they are now breaking down quickly. The Eurodollar futures curve is flattening out. The June/Sept inversion is down to just 6.5 basis points, down from 17 bps at the last FOMC meeting.

If Powell agrees to just 25 bps this meeting it will be far harder for him to go back to 50 bps in the future, regardless of the inflation data, the economic data or whatever.

Blood will be in the water and the sharks will circle. He will give the ECB a lifeline it doesn't deserve. 25 bps doesn't serve any interests that overlap with the Fed's survival (including the Neocons hellbent for war with Russia who want to starve the world, esp. Europe, if you believe the Fed is doing the MIC's bidding here).

This is the conundrum the Fed is facing. And the question in front of us is whether the Fed's priorities have shifted now that they have cleared the decks for their QT program. Powell has forced Davos trolls like Treasury Secretary Yellen to fight his policy and Lagarde into managing credit spreads and admitting she's failed to contain inflation.

The goal is still the return of the Fed to the center of US dollar monetary policy otherwise this paves the way for Davos' desired outcome of MMT to oblivion, fueling another round of war and famine, akin to the 1930's, and the end of national sovereignty as we've known it.

This is why it's not singularly about fighting inflation, as El-Erian framed it. That's the 'normie' position, the cover story. While inflation is a big deal for the Fed keeping its credibility it also is trying to thread the needle of geopolitics, de-dollarization of the Global South, collapsing ephemeral credit markets built in its name while not destroying capital formation at home.

No mean feat that. I don't think they will fully succeed but neither do I think they need to. Having flushed everyone's biases out into the open, they have the option of shifting priorities for a few weeks, again until the inflation data gives them the cover story to resume their 'higher rates for longer' policy stance.

And, while I'd like to be right next week and see a 50 bp hike. If they go 25 it is not the end of the world for the Fed. It just means a they have their work cut out for them regaining some lost credibility.

It does, however, open up the possibility of coming back in March with the biggest, "I told you so" in the history of monetary policy. In other words, it will give Powell the opportunity to say, "Look, I gave you what you wanted. And look where it got us."

Do you think that narrative isn't being prepped now? Last week Fed Whisperer Nick Timiraos assured us it was 25 bps this month.

This weekend he warned that FOMC members are worried about inflation returning with a vengeance later this year.

Two weeks ago the ECB was convinced rate hikes were over. Then the inflation data came in. Now it's back-to-back 50 bps from Lagarde.

In this environment, one created by using Austro-libertarians as useful idiots to oversell the Fed's incompetence and evil, Davos has made the Fed everyone's scapegoat.

No matter what happens the Fed will be blamed for the fallout now.

It's actually quite brilliant but it's also easily countered.

All Powell and company have to do is ignore the market's wishes and follow through on what they started.

So, Jay, Boobie, if you're listening.

Go 50 and signal another 50.

Go big or go home, you know, as the kids say.

Reprinted with permission from Gold Goats 'n Guns.