March 10, 2023

This article examines the relationship between credit and its anchor in value. Today, that anchor is fiat currency, which is both parochial and unstable. Historically, and in law it has always been gold.

It is a common error to think of credit in a narrow sense, without realising that officially recorded credit in the form of banknotes and deposit accounts with the commercial banks are only a minor part of the total credit in an economy. This article takes a holistic view of credit.

The relationship between credit and whatever provides an anchor to its value is a far larger topic from that commonly discussed in economic journals. It involves an understanding of the relationships between currency credit and commercial bank credit, the consequences of which rarely occur to economic commentators.

There is evidence that changes in central bank credit have a greater impact on prices than an equivalent change in commercial bank credit - a new and important topic for our consideration.

This article draws on the history of law as it applies to banking, money, and credit. For both contemporary economists and the layman, it involves some concepts that may be novel to them. But given that they concern the very survival of contemporary currencies, they are worth making the effort to understand.

Introduction

The purpose of this article is to explain why gold anchors credit values, an anchor which is absent in the fiat currencies that seek to replace it. It is a topic over which there is considerable confusion, not least from the two dominant schools of economic thought: Keynesian and monetarist. And while Ludwig von Mises, who was more responsible than anyone else for promoting the Austrian school of economics in the US explained and denounced inflationism, his work predominantly dealt with the inflation of fiat currencies, without much examination of the second level tier of credit issued by commercial banks, other than establishing its relationship with the business cycle.

It became a short step for many followers of von Mises in America and Hayek in Britain to conclude that the cycle of bank credit is an economic evil and that if banks were forced to become banks of deposit, acting as custodians while other institutions would act as arrangers of finance, then we would abolish the credit cycle.

Clearly, the expansion of credit tends to undermine its purchasing power. But the relationship between the changes in the volume of credit and its purchasing power is not straightforward. And then there is the difference between central bank credit and commercial bank credit to consider: does one undermine purchasing power more than the other? So far as I'm aware there is no economic literature examining this possibility.

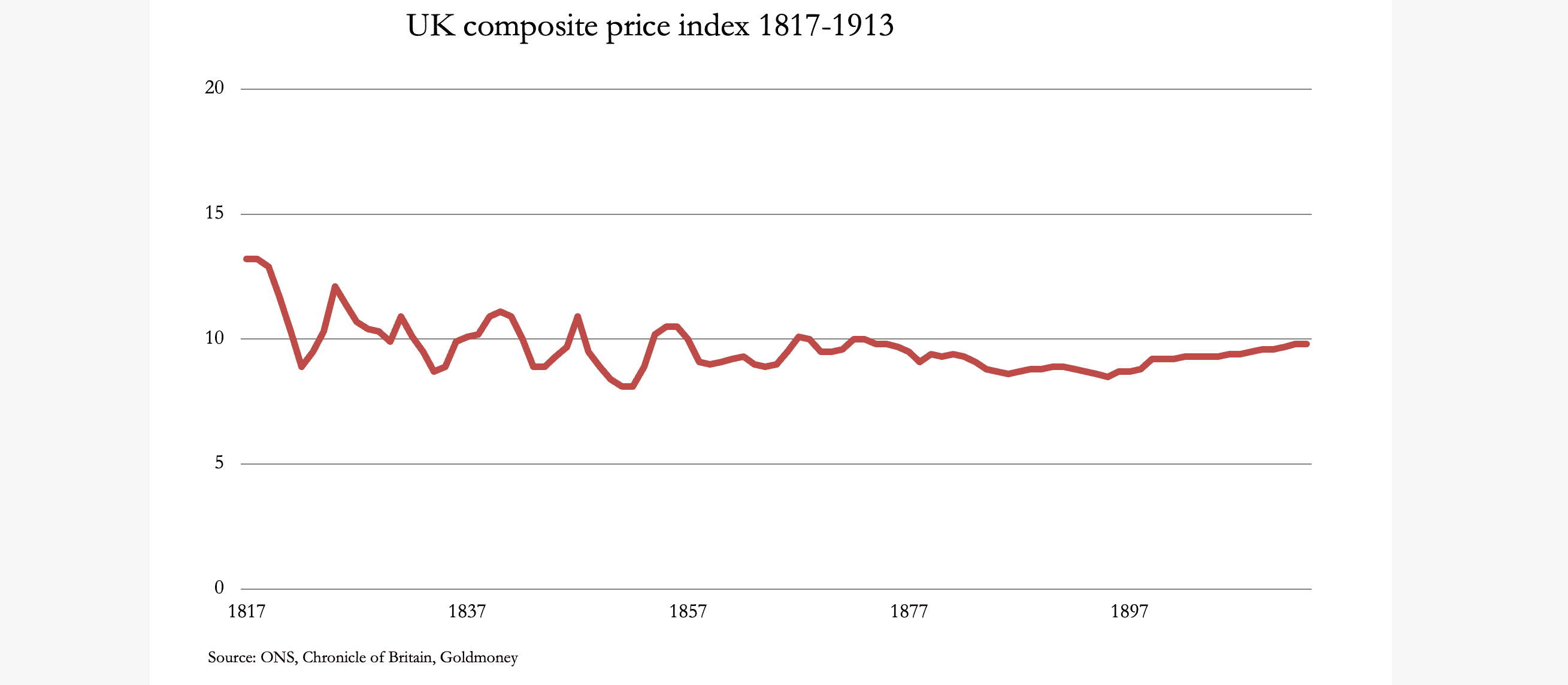

The current situation of currencies with no relationship to gold has only been in place for fifty-two years. Before that, the link was gradually eroded from Roosevelt's ban on ownership by American citizens in 1933, its revaluation in dollar terms the following year, and the Bretton Woods agreement in 1944. In has been a journey away from sound money lasting ninety years. Despite this progressive attrition, prices, particularly of commodities and raw materials were relatively stable before the ending of all links between gold and currencies. Now we should turn to empirical evidence of price behaviour under a proper gold standard, as shown in the chart below.

This is the only long run of statistical evidence of price stability under a gold standard and is of wholesale prices in the UK following the Napoleonic Wars. As usually happens, there was a post war slump as war spending ceased, reversing war-time inflation, and leading to lower prices. The gold sovereign coin standard was introduced in 1817, which continued to be exchangeable for Bank of England banknotes until the First World War. And as the new gold coin standard bedded in, the cyclical changes in price levels gradually diminished, partly due to improvements in the banking system, such as in the clearing system set up by the London banks, which was joined by the Bank of England in 1864.

Before 1914, the British government paid down most of its record high levels of Napoleonic War debt. Through industrial development, the British economy improved the living standards of the people substantially. And despite its diminutive size, Britain became the wealthiest nation in the world. As can be seen from the chart, after a shaky start producer prices became remarkably stable, barely changing in aggregate over almost a century.

The Bank of England's banknote issue, which was encashable into gold sovereigns on demand, stood at £22,082,909 in 1820. The 1844 Bank Charter Act eliminated the note issues of the other London banks, but despite their removal from circulation and after a mid-century dip the BoE's note issue only increased to £28,437,985 by 1900. Between 1844 and 1900, broad money supply is estimated to have increased by nearly eleven times and there was a substantial increase in commercial bills as well, which being credit should not be neglected. i

Despite this expansion of the quantity of credit, there was little net effect on producer price levels. In 1844, the composite price index stood at 8.9, and in 2000 it was 9.2. This suggests that an expansion of commercial bank credit has less impact on prices than an expansion of the note issue, and that not all forms of credit are equal in their effect on prices.

It is worth pausing for a moment to let that sink in. In terms of its effect on purchasing power, it has been demonstrated that changes in the quantities of bank and other wider forms of credit have significantly less impact on the general level of prices than changes in the quantity of central bank credit.

But we must introduce a caveat: the expansion of bank credit and commercial bills in nineteenth century Britain did not generally provide finance for consumption, thereby inflating prices. Today, instead of gold we are all on a loose dollar standard with respect to its role as the principal reserve currency and its function for pricing commodities and international transactions. And without gold's steadying influence, the principal factor in the relationship between gold, a currency, and subordinate bank credit is how peoples' perceptions change when credit expands. This is particularly true when credit expansion funds consumer spending.

If consumers spend the additional credit, they will tend to drive up the general price level measured in the currency. If they save it, they will tend to drive up the level of capital available for investment, benefiting manufacturing methods and thereby introducing a contrary factor which should restrict rising consumer prices. Furthermore, changes in the application of credit between purely financial activities and the non-financial GDP economy contribute to making long runs of price data misleading for assessing the impact of increases in the quantity of credit on the purchasing power of a circulating media.

In determining how the circulating media is valued with respect to the goods and services being exchanged, we cannot ignore their application to the ancient classifications of wealth. Aristotle made the connection thus: "We call wealth all things whose value can be measured in money" (Nicomachean Ethics Book V). The true meaning of wealth is exchangeable rights. And economics, or commerce, is basically the science of exchangeable rights.

There are three types of exchangeable rights which might be bought, sold, or exchanged:

- Material property or the right to it, being a specific material substance, which in law is referred to as corporeal property, alternatively referred to as material wealth.

- Immaterial property, being an individual's intellectual and labour capacity to render any sort of service. Corporate goodwill falls into this category.

- Incorporeal property which is neither material nor immaterial. It is in the broadest sense represented by debt, which is synonymous with credit, obligations which are exchangeable and are therefore wealth. It may be in an individual's possession, not yet in an individual's possession, or may only exist at a future date, such as the right to an income stream. But the right to it when it does come into existence is present and may be bought and sold just as if it was a material property. In Roman and English law, incorporeal property is a right separated from any specific corpus.

It can be immediately observed that gold coin in possession is material, or corporeal property, while credit, being a promise or obligation, is incorporeal. But the value of items, either being personal or collective wealth, in all three categories must be expressed in a medium of exchange. If that medium is a material property, it is a completely different thing from being incorporeal.

Under a gold standard, incorporeal property took its value from a material property. Under today's fiat dollar standard, all forms of incorporeal property take their value from another incorporeal property, banknotes, which are a central bank's liability. Credit is only valued in another credit, an arrangement which is inherently unstable, irrespective of changes in its quantity. Picking all this apart is the essence of the riddle we face.

Understanding gold - real money

Since the ending of barter, various corporeal properties have been used as media of exchange, but ultimately, various communities trading with each other and other completely independent communities settled on three metals as the best stores of value: gold, silver, and copper. Of these, gold emerged in the nineteenth century as setting the common standard which incorporeal credit referred to for its value, and for which all categories of wealth took their valuation cue.

The physical properties which make gold suitable for this role are well known. Less appreciated, perhaps, is that the quantity of above-ground gold stocks has increased over time at approximately the same rate as the world's population, that is at an annual average since the Reformation of about 1.2%. And if we take its growth rate from the beginning of the twentieth century, when the rate of population growth began to accelerate, the annual growth rate in above-ground stocks doubled. Therefore, its use-value to humanity has remained broadly constant.

It is impossible to quantify the split between the quantities of gold deployed into the two principal categories - monetary and ornamental. In recent years, analysts have assumed the split to be about 60% in favour of jewellery, and 40% monetary; but there are no credible figures to back these estimates up. And most of the jewellery market is in Asia, where women regard it as wearable money as well as being ornamental. It is used by their husbands to secure credit from moneylenders and pawnshops. In that sense, gold jewellery is monetary gold in the minds of its owners.

The role of gold and silver as the most common form of money goes back to before Rome's Laws of the Twelve Tables in 449BC, when according to the juror Gaius Roman coins were first introduced. The Twelve Tables were the foundation of Roman law, consolidating earlier traditions. They were the basis upon which jurors subsequently expanded their interpretations over the centuries.

With respect to the distinction between money and credit, in the second and third centuries Ulpian and Paulus between them defined where the differences lay. Their juristic findings were incorporated in Justinian's Pandects in the sixth century. And it was from them that it was made clear that the value of credit was based on money, which was physical gold and silver. Without the value-link to gold or silver, there was no means of valuing credit, and all promises, which are the essence of credit, require to be valued.

That is still the legal position everywhere today. Justinian's Pandects were published in Latin in 530AD, two centuries after the seat of Roman government had moved to Constantinople. The courts were then exercising Roman law in Latin over a predominantly Greek-speaking population, which was obviously an unsatisfactory situation. Accordingly, Justinian's Institutes was published ten years later in both Latin and Greek by Theophilus as a textbook guide to the original Pandects, becoming the basis of civil law throughout the Eastern Empire.

In 892AD, the whole legal system was revised and consolidated under the Basilian dynasty and came to be known as the Basilica, which replaced the Pandects and the Institutes as the law of the Eastern Empire and the legal basis for money and credit as far as the Steppes and even beyond. Justinian's Roman law in Latin continued to be the basis of legal development in Western Europe. Thus it was, that the European interpretation of Roman law of money and credit spread around the world as Spain, Portugal, Holland, and Britain explored and colonised all the Americas, Africa, India, and even to the far Spice Islands and Australasia in the Pacific.

So far as I'm aware, there have been no attempts to alter the legal status of gold, only a few laws temporarily banning or restricting its use as money. Even though it doesn't feature as such in modern economies and economics, gold still remains the principal corporeal form of medium of exchange.

Defining credit

Most people probably think that credit evolved after money in the form of coin, but that is incorrect. Credit existed long before, defined in the value of deliverable goods. A thousand years before Rome's Twelve Tables, the Phoenicians traded throughout the Mediterranean and even as far as Cornwall, where they procured valuable tin. The Phoenicians would have had the same problems faced by businesses today. In order to undertake their trading ventures, they required credit, because they faced expenses before they returned from their voyages many months later with vendible products.

As Demosthenes, the Greek orator and statesman, contemporary of Philip of Macedonia and his son Alexander at the same time as Rome promulgated the Twelve Tables put it:

"If you were ignorant of this, that credit is the greatest capital of all towards the acquisition of wealth, you would be utterly ignorant". ii

Perhaps even more so today, we rely on credit for every aspect of our lives. Legal money is hardly ever used - never in the major advanced economies. But even in the past, it was subject to Gresham's Law, hoarded and not spent.

Credit is synonymous with debt. It's not just that we have banknotes and token coins (representative credit), and bank accounts (credit whether you are a depositor or borrower). But when you employ a workman, you enter into an obligation to pay him, which is your debt for which he allows you a matching credit until you discharge the obligation with another credit, either in the form of banknotes or a transfer of your credit at a bank to a credit at his bank. Alternatively, you might buy an airline or rail ticket in advance. You pay with your credit at your bank and the airline or rail company credits you with an obligation to provide a service at a future date. If you promise your son that you will pay his university fees and give him an allowance, you are entering into an obligation, the promise of credits to cover his or her future debt obligations for as long as he attends the university. Every transaction, every promise, every guarantee, involves incorporeal credit with matching debt obligations. Demosthenes certainly had a point.

The distinction between corporeal money and incorporeal credit is that the former exists physically, and the latter is always created between consenting parties. The commentators who argue that bank credit should be banned appear to be unaware of the true extent of credit in the economy, and the inequity and futility of banning dealers in credit, which is the function of a commercial bank. Not only would nearly all trade cease, but a police state of the most draconian sort would be required to enforce it. And the monetarists who believe that money supply statistics define all the circulating media when they are just the tip of a far larger credit iceberg are also in error.

But debt and credit must take its value from something. At one level, it takes its value from a promise to deliver something else - a corporeal, immaterial, or other incorporeal property. But that assumes the purchasing power of credit is anchored against something else. In history, the value-anchor was always a corporeal entity such as gold. Instead, today it is anchored to another incorporeal asset - central bank credit, or banknotes. In other words, the entire structure of national credit hinges on the government's credibility as issuer of currency obligations.

Furthermore, each jurisdiction has credit values which refer to different currencies, diverse incorporeal liabilities in the form of central bank banknotes. A common corporeal gold standard is replaced by potentially incorporeal chaos.

While the potential for chaos in credit values now exists, credit based on government credibility can function for a considerable time. But we must recognise that the politicians have high demands placed upon them which inevitably leads them to debauch the currency as a means of surreptitiously transferring wealth from the citizenry to the government so that it can discharge its obligations. In the last eighty years, they have even made a virtue of it, claiming variously that the quantity of credit should be expanded to stimulate economic activity, to ensure prices rise at a two per cent rate to bring forward consumption, and to artificially cheapen borrowings at the expense of savers. Slowly but surely, the inflationists have descended into the economics of unreason.

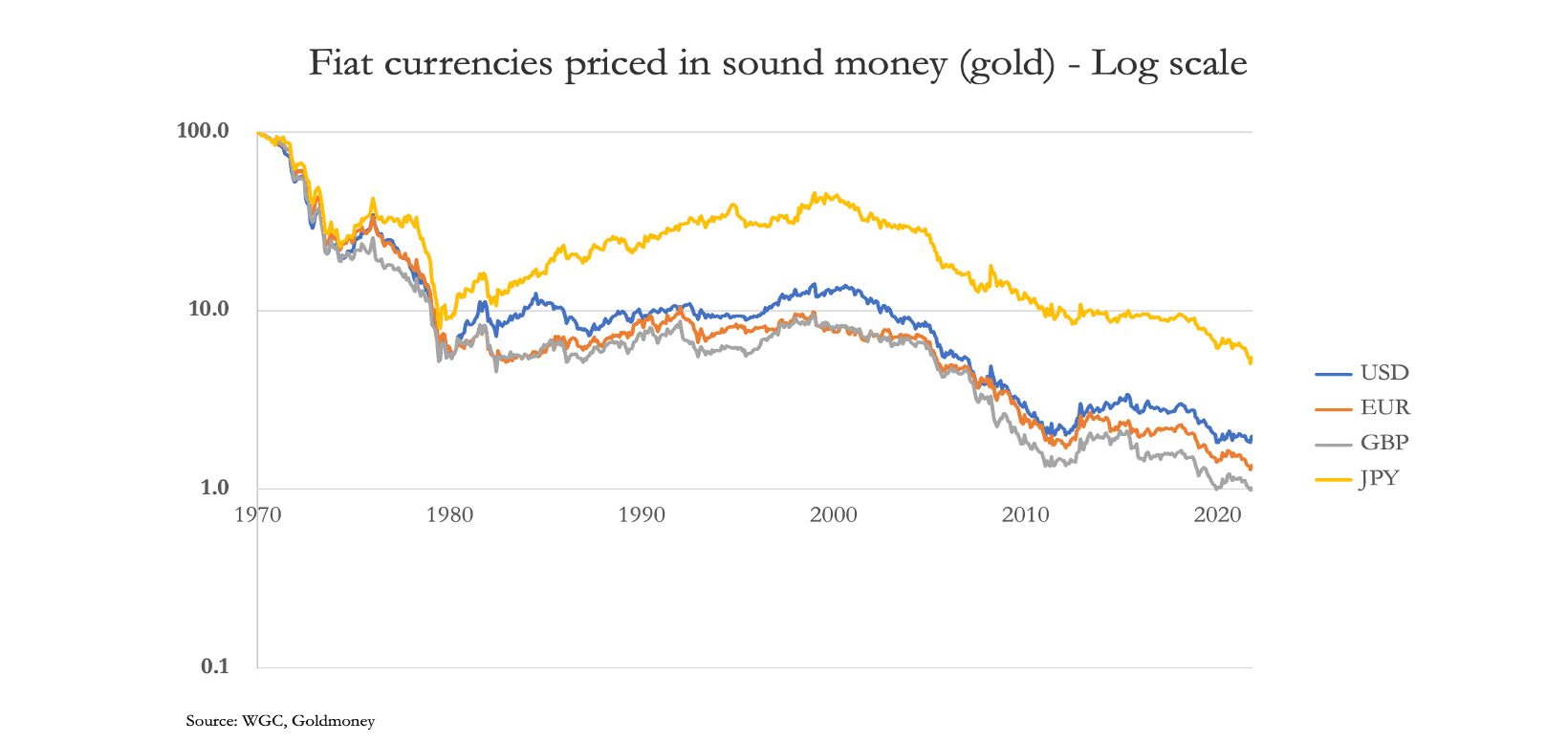

The effect on credit's purchasing power relative to gold is illustrated in the chart below, which is of the major currencies' purchasing power relative to gold, since the last vestiges of the link was abandoned by suspending the Bretton Woods agreement.

The dollar has lost 98% of its value relative to gold, and sterling has lost 99%. These currency debasements are measures of the loss of the value of subordinate credit so far under a fiat currency regime. Every transaction, every promise of a transaction, and every commitment to a future transaction has been devalued and will continue to be devalued so long as credit remains detached from corporeal money, which is gold.

The future course of credit values

It is no longer controversial to claim that the issuers of the major currencies have arrived at a crossroads. Having tried to use monetary stimulation on an unprecedented scale to prevent their economies from the adverse consequences of covid lockdowns and then the political decision to isolate Russia from global trade, the general levels of consumer and producer prices have begun to rise sharply. Consequently, interest rates have started to rise with them, threatening to drive the economies of the major currencies into an economic slump.

Now that the purchasing powers of currencies and associated credit are declining at an accelerated rate, interest rates should be allowed to find a level at which confidence in their purchasing power is restored. But that is likely to mean yet higher interest rates, to fully compensate foreign holders of these currencies for both credit risk and loss of purchasing power. We can safely assume, for the moment, that domestic holders of a currency and its dependent credit are less aware of the consequences of debasement than foreign holders who have only a speculative need for it.

The consequences of higher interest rates will be to increase the liabilities of socialising governments and accelerate the rate of currency debasement. They face debt traps which are now inescapable. The rate of loss of purchasing power for major currencies is bound to accelerate, because dealers in the foreign exchanges have become more aware of the debasement issue, giving them no alternative to retreating into their currencies of account or disposing of foreign currencies for corporeal goods, just to be rid of them.

Higher interest rates, to protect a currency from selling in the foreign exchanges, are expected to undermine financial asset values and lead to bankruptcies in the non-financial economy as business plans are thrown into chaos. This has now become obvious to everyone with interests in financial markets, which is why domestic investors less sensitive to the currency issue than foreigners, hope that their central bank will follow an alternative course, of cutting interest rates and resuming quantitative easing to stop their economies from entering a recession.

But it is these reflationary policies that led to a widening gulf between corporeal gold and incorporeal credit in the first place. Doubling down on these policies will merely accelerate the collapse in purchasing power for incorporeal currencies. It seems that whatever the policy outcome, whether interest rates are permitted to increase or remain heavily suppressed, residual confidence in the major currencies is about to face a major challenge.

The solution is now politically impossible

The only solution to prevent fiat currencies from collapsing entirely is to officially recognise and reintroduce gold as money, making it the standard against which all credit is valued. Making the arrangement stick then becomes the issue.

There is no point in simply declaring some sort of link between a currency and gold without reforming the role of central banks and their governments in the economy. Central banks should let markets set interest rates, which both central banks and investors will strongly resist.

As well as monetary policy reform, it has to be decided what fiscal reforms are required and what the limitations on the roles of a government should be. To understand the issues involved requires the entire government establishment to recognise the errors in economic policies which have become received wisdom since the Second World War. Textbooks on Keynesianism, which repeat all the dogmas of John Law, must be destined for the curiosity shop. And those on monetarism, which inappropriately failed to adapt to accommodate the introduction of fiat currencies and detached credit should suffer a similar fate. Governments must understand that meddling in economic matters best left to transacting individuals only guarantees economic decline.

Accordingly, with a return to corporeal money they must introduce legislation to rescind the large majority of welfare obligations. They must get out of the healthcare and education industries, devising alternative arrangements for those genuinely in need. They must rescind regulations instructing how businesses run themselves, and the standards they and their products must comply with. They must reduce their burden on the economy to less than 20% of GDP -10% would be even better. They must not permit budget deficits. They must not permit industrial lobbying. They should restrict their activities to ensuring criminal and civil laws are respected, the latter providing a clear framework for contract law. They must provide national defence. On foreign policies, they should not interfere in other nations' affairs except to the extent they involve their own national interests. They should remove restrictions on trade...

The purpose of listing some of the reforms in government and its relationship with the wider economy necessary to ensure that a new gold standard can endure is to illustrate the enormity of the task. No politician has a mandate even to consider moves in the required direction. It involves both the political and permanent establishments relinquishing power. It requires a renewed understanding that the state is the servant of the people, not its master. None of this will happen willingly. This is why every fiat currency, which becomes an increasing source of government finance, eventually collapses. It is the ultimate long cycle of boom and bust.

It's sliding towards either WW3 or gold

We have seen that before the First World War, the major currencies, principally being the UK pound and the US dollar, were on successful gold standards. The general view in government was that free markets provided improved living standards, and that a government's role in an economy was a burden upon it which must be kept to a minimum.

Clearly, for the major currencies a willing return to these conditions is practically impossible. But a new threat to the status quo of fiat currencies has arisen from developments in Asia, which as a whole is more dependent on production than purely financial activities. This is in sharp contrast to the US and UK which have become particularly dependent on credit for credit's sake.

Under the aegis of Russia and China, the entire Asian continent with the exception of a few allies of the western alliance in South-East Asia is now focused on creating an industrial revolution, replicating the success of nineteenth century Britain. And the planners involved appear to recognise that a sounder money than a fiat dollar must be an integral part of it.

As well as seeking to do away with using the dollar for facilitating currency transactions and pricing commodities and raw materials, these Asian nations appear to be gravitating towards linking their currencies to a corporeal standard. More specifically, Sergey Glazyev, the head of the Eurasian Economic Union considering the matter has been tasked with designing a new currency specifically for the purpose of cross border transactions and for commodity pricing. From an initial concept first made public in April last year, this has been refined to an understanding that the new currency should be linked to gold, basing it on a reversion to the status quo ante.

We cannot know the true level of understanding of monetary affairs in the mind of Mr Glazyev, but both he and President Putin have demonstrated a sound knowledge of the weaknesses of the western alliance's fiat currencies. In common with China, Russia is now prioritising gold mine output, building her physical reserves to replace fiat currencies made worthless by sanctions. Glazyev is also involved in beefing up Moscow's gold exchange and Asian central banks are also accumulating gold reserves.

The nations involved are wider than the membership of the EAEU, incorporating the Shanghai Cooperation Organisation, and the growing BRICS+. Directly, states governing some 3.8 billion Asians are parties to the SCO, with perhaps a further 1.5 billion in Africa and South America becoming economically dependent or interested as affiliated suppliers. America is now leaning heavily on all nations where they have influence in an attempt to persuade them not to join the Asian hegemons' sphere of influence. She is also escalating military attacks via NATO through Ukraine on Russia and is now raising the rhetoric level against China over Taiwan and her alleged provision of weapons to Russia. It is a three-pronged attack, threatening to escalate out of control by an increasingly desperate America towards a third world war.

There is now an urgent need for Russia in particular as well as her close allies, not just to protect their currencies from the fallout of a western alliance currency crisis, but to actively undermine the dollar. The groundwork for this action is being laid down by Glazyev's plans for a trade settlement currency, which on the information available is almost certainly going to be of credit linked to gold. Furthermore, at the St Petersburg International Economic Forum last June, Putin signalled to attending official government delegations that dollars and euros should be sold, and gold stored in vaults under the control of the western alliance's central banks should be repatriated.

Not only have the central banks and governments of the entire EAEU, the SCO, and BRICS+ been put on notice to sell their currency reserves, but they will shortly have available a new trade currency based on gold to replace them. For Russia, the only way to avoid WW3 being nuclear is to fight it on financial grounds.

There are significant advantages to a trade settlement currency based on gold. As to the basic design, I refer the reader to my article dated 23 February for Goldmoney, under the section headed, "The Good". Some further comments on the currency's design in the context of credit are appropriate.

Classes of credit will be separated into three distinct categories. There is the high-level credit which only exists between participating national central banks and a new central bank set up specifically for the purpose. The currency is a liability of the new central bank issued on a simple formula of 40% backing of physical gold submitted by participating central banks. Participating central banks obtain the new gold currency in proportion to the gold which they individually transfer to the new central bank. And it can be freely redeemed or added to by participating central banks on this formulaic basis. The new currency would be available to replace the foreign currency reserves currently held by participating central banks, which would in large measure become redundant. Doing away with the need to hold significant amounts of dollars or euros addresses the currency sanction threat which Russia experienced this time last year.

The second level of gold-linked credit is between participating central banks and their licenced commercial banks. These would be the gold currency reserves equivalent to the fiat currency bank reserves we are familiar with in today's monetary systems. The reserve facility would also open the possibility for a national central bank to set reserve levels, should it wish to do so, and to participate in clearing systems, providing credit liquidity should they so desire.

The third level of credit is that created by commercial banks to facilitate trade settlements and commodity purchases by private sector actors. Commercial banks of all nations can participate should they wish to do so, either by being licenced by a participating central bank, or by holding physical gold to secure its own credit values. In this case, a bank such as JPMorgan would effectively turn their unallocated gold account facility into a deposit account linked to demand for trade finance, instead of being a vehicle predominantly used for financial speculation.

The advantages of this new trade currency system is that it leaves individual central banks to manage their own monetary policies as they see fit. Therefore, it would not require political endorsement. And as I have demonstrated earlier in this article, with the top level of credit being sound, a general expansion of commercial bank credit denominated in the new currency will have little or no effect on price levels. And it is unlikely that it will be made available by commercial banks for financing consumer spending.

The timing of Russia's escalation of the war against the dollar is likely to be advanced by America's three-pronged attempts described in the preceding paragraphs. Not only will market pressures on fiat currencies then lead to higher interest rates and bond yields undermining western capital market values, but the announcement of a new trade currency based on corporeal gold is bound to draw unwelcome attention to the weakness of commercial bank credit referring for its value to unstable central bank credit.

At the last count, foreign ownership of dollars and dollar-denominated financial assets totalled about $30 trillion, somewhat more than the US's entire GDP. For the eighty-one government delegations attending Putin's St Petersburg Economic Forum, it will rapidly become a case of sell while they can.

i See The Bank of England, 1694-2017, by Charles Goodhart, LSE Research.

ii Quoted in HD Macleod's The Theory of Credit. I cannot find his source.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated.