May 17, 2024

The consequence is soaring, unproductive debt both in public and private sectors. In the past, debt levels have been low enough for central banks to force through further interest rate suppression to perpetuate malinvestments. That is no longer possible, with G7 government debt to GDP ratios commonly exceeding 100%. This article argues that interest rates will not fall materially, if at all, but will continue to rise.

Rising interest rates threaten to destroy the stagnating businesses which make up most of G7 economies, threatening entire banking systems. As their power has increased, central banks now bear responsibility for the financial integrity of the business environment as well. Individual insolvencies may be tolerated, but the prospect of wholesale failures requires governments and their central banks to prevent them.

Consequently, Schumpeter's concept of creative destruction has not been permitted to work its magic, and without which capitalism fails to deliver economic progress. We are usually aware of the economic progress arising from new technologies because it is plain to see. But we are less aware of the need of more mundane processes to continually evolve. In free markets this is achieved by competition among suppliers to improve products and services for the consumer.

It follows that a Darwinian process of natural evolution must occur, whereby those businesses not fit to survive competition must die, and their capital and labour resources redeployed towards production that is viable and capable of anticipating ever-changing patterns of consumption.

Before addressing the consequences of interest rate policy by which central banks support failing businesses, we should note that there are other factors standing in the way of wider economic progress. Big businesses lobby governments for trade protection and subsidies, which are anticompetitive and suppress rivals. Trade tariffs and quotas remain a popular way of protecting domestic markets from foreign competition, readily labelled unfair. The entire structure of regulation is designed to keep establishment businesses going and upstart competition out. This is achieved by the state effectively taking purchasing decisions out of the hands of consumers by insisting that only approved goods and services are available to them.

For some time now, the business of government and central banks is to protect and perpetuate corporations which can no longer compete in free markets. Politicians and government economists compound the problem by being unaware that their policies are anti-progress. Instead, they talk of economic growth measured by GDP, which is not and never can be a measure of economic progress. GDP is simply the total of credit deployed in the transaction of qualifying items. It provides excellent camouflage for zombies.

GDP growth is merely the inflation of credit. And it is the availability of credit at low interest rates which is central to the survivability of zombie corporations. The reason this is the case is because high interest rates penalise time wasted, while low rates less so. Suppress interest rates and dealers in credit, which are the banks, are less worried about the bad debt consequences of extending credit. Raise interest rates and it obviously becomes an issue of lending risk. The relationship between credit and interest rates is why the kneejerk response to a recession is for a central bank to reduce interest rates.

A problem with official interest rate policy is to know what rates should be. The answer, of course, is that they can only be decided in markets where participants price time-preference and credit risk. But when a central bank intervenes it cannot be guided by this knowledge and is flying blind. Policy takes over, and policy always dictates that a level should be set which is stimulative to the economy, evidenced by an expansion of credit - hence the GDP measure.

The use of interest rate policy to stimulate credit creation has resulted in a continual suppression of interest rates since the 1980s. This followed the instability of the 1970s, after which the Fed under Paul Volcker raised the Fed funds rate to 19%. Since then, they have declined eventually taking the time preference factor out of debt entirely, as the chart below of the Fed funds rate shows:

We can only guess when the zombie problem began to develop in earnest. But it is worth noting that following the 1981 peak in the funds rate, the recessions marked by the shaded bars always accompanied falling interest rates. An economist will tell you that in a recession falling rates are justified to stimulate demand for credit. But a banker will tell you the opposite: in a recession there is greater lending risk and rates should rise to compensate.

A banker is dealing with risk, while an economist justifies official policy. For the last forty years interest rates have fallen at times of recession providing clear evidence of interest rate suppression, which can only be aimed at perpetuating businesses which would otherwise be taken out by Schumpeter's creative destruction.

The chart runs to 2022, after which the Fed was forced to raise rates to the current target level of 5.25-5.5%. This has already driven a few banks into insolvency, and in the wider private sector other businesses which became reliant on interest rate suppression, such as commercial real estate, are also faltering. The living-dead in the US economy are finally marching towards their graves.

The widespread anticipation is for the Fed to return to interest rate suppression, particularly by those whose business survival depends upon it, as well as the investors whose portfolio valuations stand to benefit. But inflation seems reluctant to go away, forcing the Fed to retain higher interest rates for longer. And higher prices are still being driven by the dilution of the currency through a rising government budget deficit. I estimate the current fiscal year's deficit to end-September including debt financing costs will be over $3 trillion, inflating the quantity of credit reflected in a nominal GDP of about $28 trillion accordingly, certain to be reflected in continuing price inflation.

Keynesian economists who dominate macroeconomic thinking in capital markets believe that interest rates must fall to prevent a recession. But they ignore the position of bankers whose balance sheets are over leveraged and are acutely aware of duration risk. The following is extracted from Jamie Dimon's Letter to Shareholders in JPMorgan Chase's 2023 Annual report:

"[Equity] markets seem to be pricing in at a 70% to 80% chance of a soft landing - modest growth along with declining inflation and interest rates. I believe the odds are a lot lower than that...

"...we are prepared for a very broad range of interest rates, from 2% to 8% or even more, with equally wide-ranging economic outcomes - from strong economic growth with moderate inflation (in this case, higher interest rates would result from higher demand for capital) to a recession with inflation; i.e., stagflation. Economically, the worst-case scenario would be stagflation, which would not only come with higher interest rates but also with higher credit losses, lower business volumes and more difficult markets." (italics are mine)

Given the extracts which I have italicised, almost certainly Dimon expects higher interest rates "perhaps of 8% or even more", and that expressing it as a range from 2% upwards is not his real view. Otherwise, his expectations are those of a banker who knows not only that higher interest rates are inevitable, but also the damage it will do to swathes of overindebted businesses owing money to his and other banks.

So what does a banker do in these circumstances? He reprices risk. He lobbies for government support for ailing businesses, bailouts to avoid having to write off non-performing loans. That is the subtext in Dimon's letter.

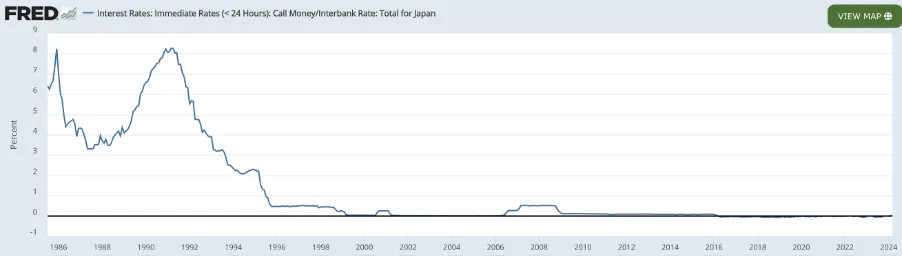

Japan's rate suppression

The US is not the only zombified economy, and Japan's case is even more obvious. Ever since Japan's stock market crash of 1990-1991, the Bank of Japan has suppressed interest rates. Initially, that suppression was centred on rescuing Japan's commercial banks which were ruined by the deflating asset bubble.

With the banking system's bankrupt condition kicked into the long grass, the rest of what became described as the lost decade didn't see the revival of asset values that suppressed interest rates were meant to encourage. In a Keynesian-inspired effort to revive economic activity, interest rates were reduced to zero, and made negative from the late 1990s onwards. This is illustrated in the chart of overnight interbank rates below.

Not even that worked. So, from 2000 onwards the Bank began injecting raw credit into the economy by buying in government debt, a move which was later dubbed quantitative easing in the wake of the Lehman crisis in 2009. Having adopted a 2% inflation target, which was plainly unsuited for an economy with a stubbornly high savings rate, the BOJ has persisted with these failed reflationary policies ever since.

Consequently, the entire economy of domestic Japanese businesses and their bankers have become dependent on a combination of zero interest rates and excessive government spending. The government has run annual deficits of as much as 10% of GDP, averaging over 6.5% since 1992, leaving it with a debt to GDP level of over 250% of which nearly 60% is owned and monetised by the Bank of Japan.

Not only is the entire private sector zombified, but the government and the Bank of Japan are as well. They simply cannot survive a return to interest rate normality.

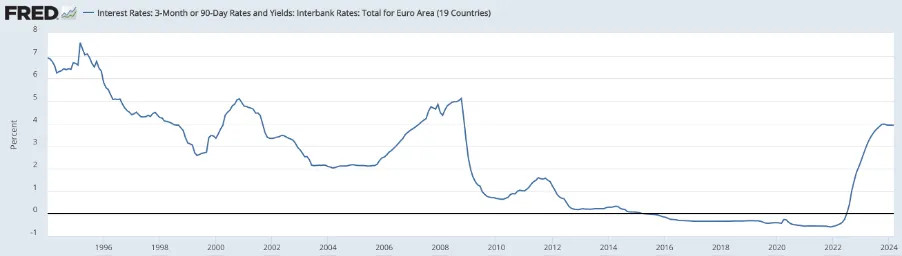

The euro area is similarly afflicted

From the chart above, it is obvious that the Eurozone has also been in the business of interest rate suppression. But this conceals a further deliberate zombifying effect. The euro system reduced borrowing costs in the PIIGS (Portugal, Italy, Ireland Greece, and Spain) by converging them all downwards to a common euro level. Under the euro umbrella, a previously yielding Italian corporate bond of perhaps 12% would fall to under 4%. So not only was the ECB suppressing interest rates since the euro's inception in 2000, but the distortions in the PIIGS were even greater.

In the wake of the US Lehman crisis, which hit Eurozone banks hard through the transfer of systemic risk, a Eurozone banking crisis followed with Cyprus and Greece in states of collapse. Cyprus was small enough to be told to go hang. But Greece was too large to ignore, particularly since the other PIIGS acting like falling dominoes would have been next. The solution was to flood the Eurozone with credit, whereby the ECB drove interest rates negative and in conjunction with the national central banks funded ballooning government deficits by buying their debt. As we have seen in the US and Japan, this only served to preserve businesses which should have gone bust thereby releasing capital and labour resources for productive redeployment.

The sharp rise in interest rates since 2022 means the zombies cannot now refinance themselves and must fail. Theoretically, this is a good thing because the process of creative destruction can resume. But that is not to reckon with the state of the entire banking system. The eurozone's global systemically important banks have asset to equity ratios in the region of 20 times, which means they are unable to absorb the losses from creative destruction. Furthermore, with massive and increasing hidden balance sheet losses and imbalances in the TARGET2 settlement system, recapitalising the euro system poses exceptional challenges. In short, the entire euro system is bust and there is a significant risk that this manufactured fiat currency might not survive a normalisation of interest rates.

Conclusion

Between the US, EU, and Japan we can see that there is a reckoning approaching. Their elevated levels of government debt calls time on interest rate suppression as a means of hiding widespread malinvestments in their economy. The US in particular will be unable to fund itself without higher bond yields because foreigners' appetite for dollar debt is diminishing. And that is even before considering the hidden liabilities exposed in an economic downturn.

Central to this argument is the disagreement between economists and bankers over the interest rate outlook. Economists argue that an economic crisis can always be deferred by lowering interest rates and expanding credit. But that only works if a government and its central bank can impose these conditions and takes no account of the accumulating economic consequences of deferring the benefits of creative destruction.

Bankers take a different view. Greater lending risk requires less credit availability and higher interest rates to compensate for escalating risk.

Reprinted with the author's permission.