April 21, 2026

Throughout most of our history leprosy has probably ranked as one of the most horrifying human conditions.

That slow, wasting disease lacked any cure and produced hideous deformities, leading to the creation of isolated confinement colonies for the afflicted. It's hardly surprising that in the New Testament, Jesus extended his healing touch to lepers as a demonstration of his exceptional personal concern for those who were most despised by the rest of society.

According to Wikipedia, modern science has demonstrated that leprosy is caused by a bacterial infection that destroys the nerves that transmit pain. Lacking such sensations, the human body loses its warning system and therefore becomes greatly vulnerable to all sorts of minor injuries. These gradually accumulate, eventually producing the physical damage and grotesque disfigurement that represents the visible manifestation of the illness.

Pain may be unpleasant, but it serves a vital role and its absence can be extremely dangerous for an organism.

I'm sure that if test animals were affixed with drug-patches that numbed any pain sensations and then released into the wild, their life expectancies would be drastically reduced.

There is often a close analogy between biological and social situations, and the absence of painful warning mechanisms in our society and economy may be just as dangerous to our future well-being as it would be for an animal or human.

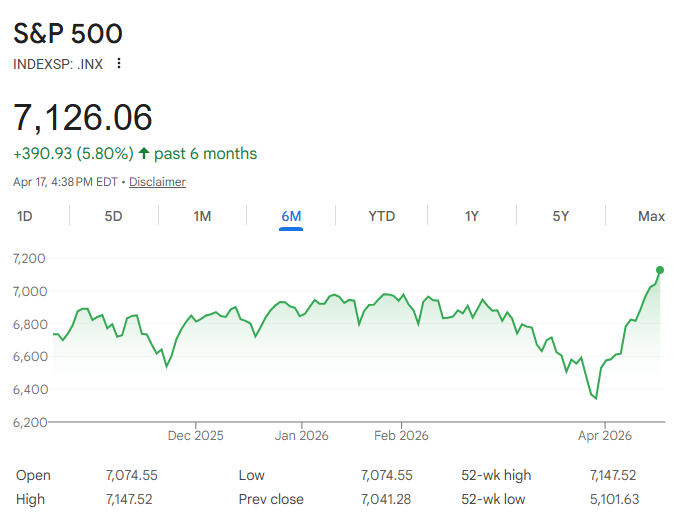

These were some of the thoughts that came into my mind over the last few weeks as I noticed the astonishing, near-total equanimity with which our financial markets seemed to be treating the American-Israeli war against Iran.

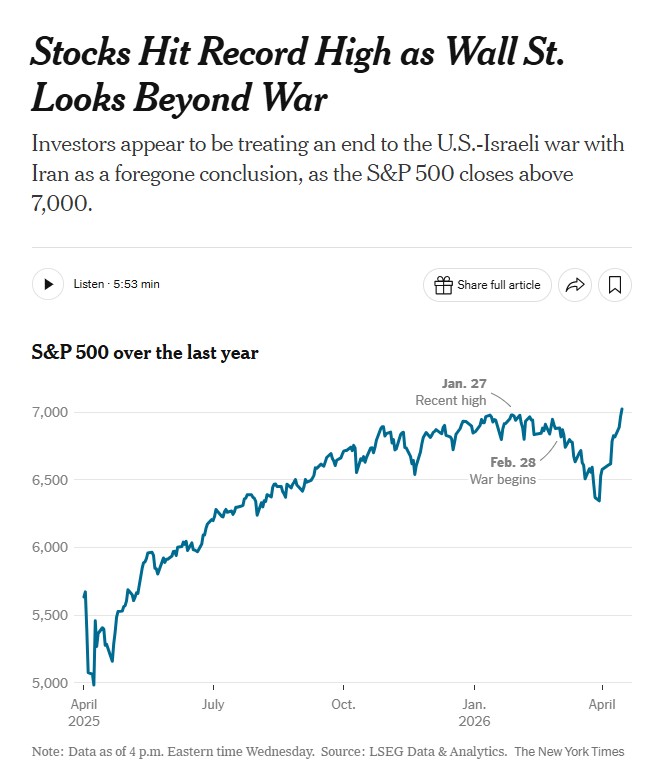

Despite temporary dips, most of our major stock market indexes such as the S&P 500 are now considerably higher than they were before the fighting began, and have even set new records. This was hardly what we might have been expected.

President Donald Trump notoriously pays close attention to stock prices, and just a couple of days ago the Times described how these soaring market values led him to ridicule those who had urged him on economic grounds to avoid a war with Iran.

He also appeared to criticize advisers who had warned him against going to war with Iran because it would affect fuel prices. He described rising costs as "fake inflation."

"We have consultants," Mr. Trump said, recounting the conversation, "'Sir, if you do this, fuel is going to go to $300 a barrel. The Depression is going to happen.' That can't happen because we just hit a brand new all-time high."

That was an apparent reference to the stock market, which hit a fresh record high this week, reflecting investors' optimism that a peace deal would be reached before the war could inflict significant damage on corporate America.

While Trump is hardly known for the accuracy of his statements and I'd never heard any talk of oil going to $300 per barrel, his remarks were otherwise reasonably correct. Financial consequences of the Iran War have so far been very different than what most analysts had expected, or still predict.

John Mearsheimer is one of our most distinguished political scientists, and someone always quite careful and judicious in his remarks. But in his interviews during the last week or so he has regularly argued that the global economy was much like the Titanic, headed straight for an iceberg. Jeffrey Sachs, an equally distinguished international economist, has said very similar things.

Others have gone even farther. Following his long career in the British Navy, Cmd. Steve Jermy became an expert on energy transport and international trade matters. A few days ago he declared that we had already hit the iceberg, with the hole only getting larger every week that that the war continues. Given the long-term disruption of global supply-chain problems, he predicted an utter economic catastrophe.

All of these seemingly knowledgeable individuals and many others have agreed that the global economy is facing its worst crisis since the Great Depression nearly a century ago, but the financial markets have emphatically said otherwise. The same day that last, very sobering interview aired, American stock prices set a new record, and since then they have risen even higher.

Trump may be an ignoramus while Mearsheimer and Sachs are outstanding scholars, but the consensus of investors is in the camp of the former rather than the latter, and surely it is foolhardy to totally disregard the views of those who put their money where their mouth is.

So we currently have two radically different perspectives on the global economic situation, with many experts crying "Doom!" but the stock markets saying "Don't Worry-Be Happy!" and obviously only one of these predictions can be correct.

My original academic training was in theoretical physics, and according to the conventional interpretation of quantum mechanics, subatomic particles such as electrons may be interpreted as probabilistic waves, with their physical characteristics such as location or spin remaining indeterminate until they are measured. That latter process then collapses the wave function and thereby reveals where they have been and whether they are up or down. So in a very similar fashion, within a few weeks we shall discover whether all those notable experts or the aggregated wisdom of the financial marketplace was a better guide to the world's economic situation.

There are certainly important historical precedents for stock markets not reflecting a looming economic catastrophe. For example, the Dow Jones Industrial Average and the S&P 500 both peaked on October 9, 2007 just a few months before the collapse of Bear Stearns initiated the massive 2008 Financial Meltdown that produced the Great Recession, the most serious global economic crisis since the Great Depression of the 1930s.

During that ensuing crisis, both those stock indexes dropped by well over 50% during the 18 months that followed. Yet for anyone who had been paying attention, by the date of that market peak there had already been numerous early warning signs of what was about to happen, with large financial institutions and major hedge funds collapsing throughout 2007, both before and after stock prices reached their zenith. Yet at the time investors had blithely ignored all that mounting evidence.

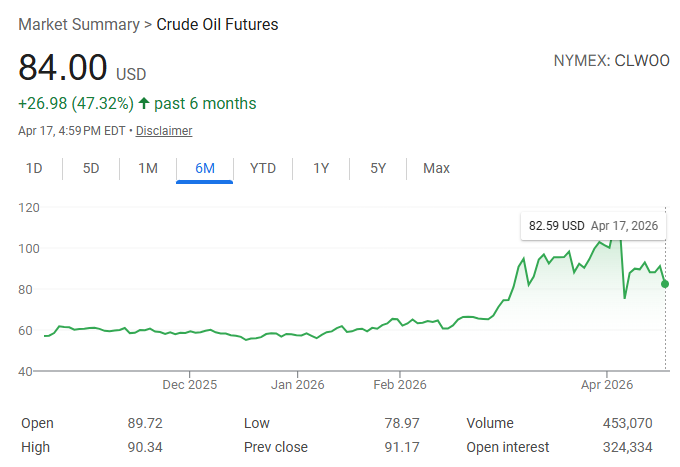

The obvious reason that traders and fund-managers have remained so insouciant is that contrary to all expectations, prices for oil and natural gas have risen much less than anyone had expected when the war began.

For example, the widely quoted benchmark price for crude oil is now only about 30% higher than the very low levels from earlier this year, showing none of the massive price spikes that had been widely predicted. So a price rise that has been rather modest and perhaps only temporary helps to explain why stocks have largely ignored the conflict.

For decades, Iran had always threatened that if were attacked it would close the Strait of Hormuz in retaliation, and it immediately did so. That strategic waterway normally carried some 20-25% of the world's oil and natural gas exports, and an even larger fraction of other vital commodities such as fertilizer.

Iran still exported its own oil and the Saudis were able to use a pipeline to redirect most of their crude to a port on the Red Sea But the Iranian blockade still took around 10 million barrels of oil per day off the world market, representing roughly 10% of total global consumption, and this was obviously an enormous, immediate shock to the system. Numerous experts had suggested that if this loss of supply continued for any extended period of time, a severe global recession would inevitably result, or even a worldwide depression.

An industry newsletter recently declared this to be "the largest energy supply disruption in modern history" and estimated that "more than 500 million barrels of crude and concentrate have been removed from the global market," emphasizing that "the world has never seen anything like this before."

It's official:We are now witnessing the largest energy supply disruption in modern history.

Since the start of the Iran War on February 28th, more than 500 million barrels of crude and condensate have been removed form the global market.

In other words, global supply has now... pic.twitter.com/E2pcjPh8yB

- The Kobeissi Letter (@KobeissiLetter) April 18, 2026

Prior to his attack on Iran, President Donald Trump had completely dismissed all the warnings of the potentially devastating economic consequences of an Iranian closure of the strait. Once it became apparent that it would be difficult or impossible to reopen that waterway to cargo traffic by military force, his administration turned to desperate measures to compensate for the sudden loss of world oil supplies.

The International Energy Agency soon declared that the Iran War was producing "the largest supply disruption in the history of oil markets." Trump officials announced that that the 32 nations in the IEA were releasing 400 million barrels of oil and refined products from their reserves, which included 172 million barrels from our own Strategic Petroleum Reserve.

America also removed all previous sanctions on Russian oil, thereby allowing countries to easily purchase it, including the large quantities that had already been exported but were sitting at sea without buyers.

Even more remarkably, we did the same to Iranian oil, thereby allowing the country we were attacking and seeking to destroy to freely market the 140 million barrels of crude they had already shipped but been unable to sell, earning Iran a potential windfall of around $15 billion, twice its annual military spending. I've never previously heard of any country during wartime taking such a step to boost the government finances of the enemy it was seeking to defeat and destroy.

Iran also began furiously pumping and shipping additional oil, selling it at much higher prices than it had previously received. Trina Parsi, a prominent Iran expert, noted that as a result the oil revenues received by the Iranian government had more than tripled from what they had been before the missiles began firing.

Energy industry insider in Iran tells me the following, and it is STUNNING:Before the war, Iran produced just shy of 1.1mn barrels of oil per day, and sold it at $65 per barrel minus $18 discount (i.e. $47)

Today, it produces 1.5mn barrels a day, and sells it at $110 with...

- Trita Parsi (@tparsi) March 23, 2026

All these factors temporarily mitigated the impact of the current supply shock that the Iranian action had produced. Some 500 million barrels had so far been removed from the market, but the releases from strategic national reserves and the removal of Russian and Iranian sanctions more than made up for those losses. Furthermore, large oil tankers often take weeks to reach their destination, so the global shortage of oil would only become fully manifest after the last tankers that had exited the Persian Gulf at the end of February unloaded their cargo and no additional ones arrived.

Taken together, this would explain why current oil prices had risen much less than otherwise expected. But we would still see a price spike in another month or two once these temporary sources of additional supply had been exhausted.

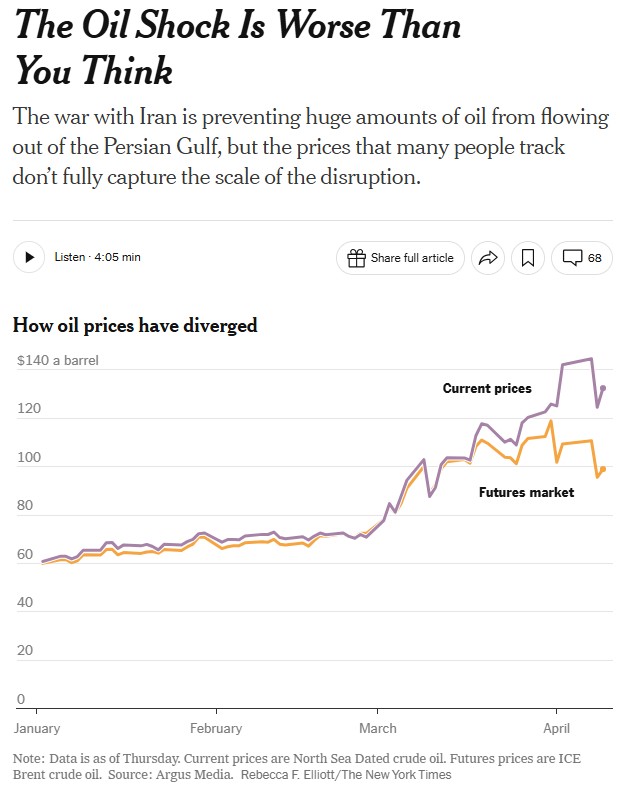

Yet oddly enough, the exact opposite has actually been the case. The headline oil prices so widely quoted in our media represent those in the futures market, the costs of a barrel of oil a couple of months down the road, while the oil prices for current, physical delivery have been far higher. For example, although future prices have periodically broken $100 per barrel, they have now fallen back down below $85. Meanwhile, the cost for the current delivery of physical oil—spot prices—have at times recently touched $150 per barrel. Indeed, a couple of days ago physical oil traded as high as $200 per barrel in Asia.

This is not a…

This gap between future prices and current prices was not only the exact opposite of what we would expect, but it was also totally unprecedented in its magnitude. Last week, I cited an important New York Times article that made this point:

On Tuesday, before President Trump said the United States and Iran had reached a cease-fire agreement, a commonly cited price of Brent oil, the European one, was about $109 a barrel. That was well below highs reached in 2022, when that price briefly topped $130, without adjusting for inflation.But in the market where energy companies buy and sell liquid oil transported on ships, the price was almost $145 a barrel, a record and more than double the price before the United States and Israel attacked Iran on Feb. 28, according to Argus Media, a company that tracks commodity prices...

"The futures market is not representing the on-the-ground and on-the-water reality of oil at all," said Vikas Dwivedi, global energy strategist at Macquarie Group, an Australian financial services firm. "It's quite broken."

Mike Wirth, the chief executive of Chevron, the second-largest U.S. oil company, expressed similar concerns last month at a Houston energy conference, CERAWeek by S&P Global.

"Physical prices and physical supplies would reflect a tighter market than I think the forward curve reflects," Mr. Wirth said, referring to the futures market.

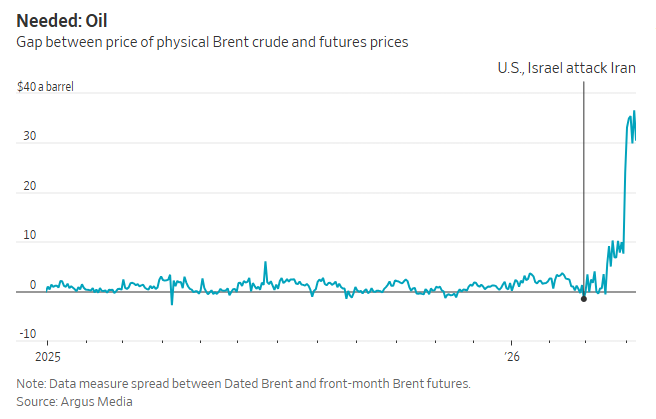

A few days later, an article in the Wall Street Journal told the same story of the strange, massive gap that had suddenly appeared between "fictional" and physical oil prices:

Prices for cargoes of oil for near-immediate delivery are trading at an unprecedented premium to futures contracts that deliver crude in two months' time. As of Friday, they stood $31 a barrel higher than front-month Brent futures contracts, a historical anomaly that points to desperation among oil importers.Buyers are also paying unusually high premiums to get hold of jet fuel and diesel straight away.

"Refiners are looking for oil wherever they can get it," said Ole Hansen, a commodity strategist at Saxo Bank in Copenhagen. "A lot of bids are not getting answered."

Actual users of petroleum products operate on physical rather than fictional oil so a recent CNBC article carried the headline "Europe could run out of jet fuel in 6 weeks, IEA warns":

Europe may have just six weeks left of jet fuel, with serious consequences for the continent's economy, the International Energy Agency warned on Thursday...Earlier, IEA Executive Director Fatih Birol said the Strait of Hormuz blockade will result in "the largest energy crisis we have ever faced," in an interview with The Associated Press on Thursday.

He added that the broader economic impact includes "higher petrol (gasoline) prices, higher gas prices, high electricity prices," with some parts of the world "hit worse than the others."

Birol previously warned that the energy crisis was set to hit harder in April as oil supply constraints worsen.

"In April, there is nothing," Birol said last month. "The loss of oil in April will be twice the loss of oil in March. On top of that you have LNG and others. It will come through to inflation, I think it will cut economic growth in many countries, especially emerging economies. In many countries the rationing of energy may be coming soon."

That same day, a WSJ article explained our own domestic airlines had also been very hard hit by skyrocketing jet fuel prices, which had doubled from what they had been last year.

Perhaps I'm being overly conspiratorial, but many Zionist billionaires are determined to continue the war and they have a powerful incentive to temporarily mask the terrible economic consequences of the Iranian blockade of the Strait of Hormuz. So I wonder if they aren't manipulating the widely-quoted futures market prices, which might otherwise have already panicked Wall Street and forced Trump to end the conflict.

Applying another biological metaphor, if someone is suffering very serious, life-threatening injuries, injecting him with pain-killers and euphorics may hide most of his symptoms without alleviating the deadly underlying condition.

Trump may or may not have recognized the magnitude of the global economic catastrophe that seemed to be rapidly approaching, but by the beginning of April he must have realized that his Iran War had not been the great success that he had originally envisioned.

His commanders had apparently persuaded him that they had no means of reopening the Strait of Hormuz through military force and that any attempt to do so would probably result in very heavy American casualties.

Trump was desperate for an end to the war but he refused to accept the humiliation of admitting defeat, so he sought some face-saving victory that could be used to mask his retreat.

That probably explained the apparent commando-raid he launched to seize Iran's enriched uranium. But the operation ended in total disaster, with a dozen American aircraft destroyed and their wreckage strewn across a temporary airfield near Isfahan and the Natanz nuclear site.

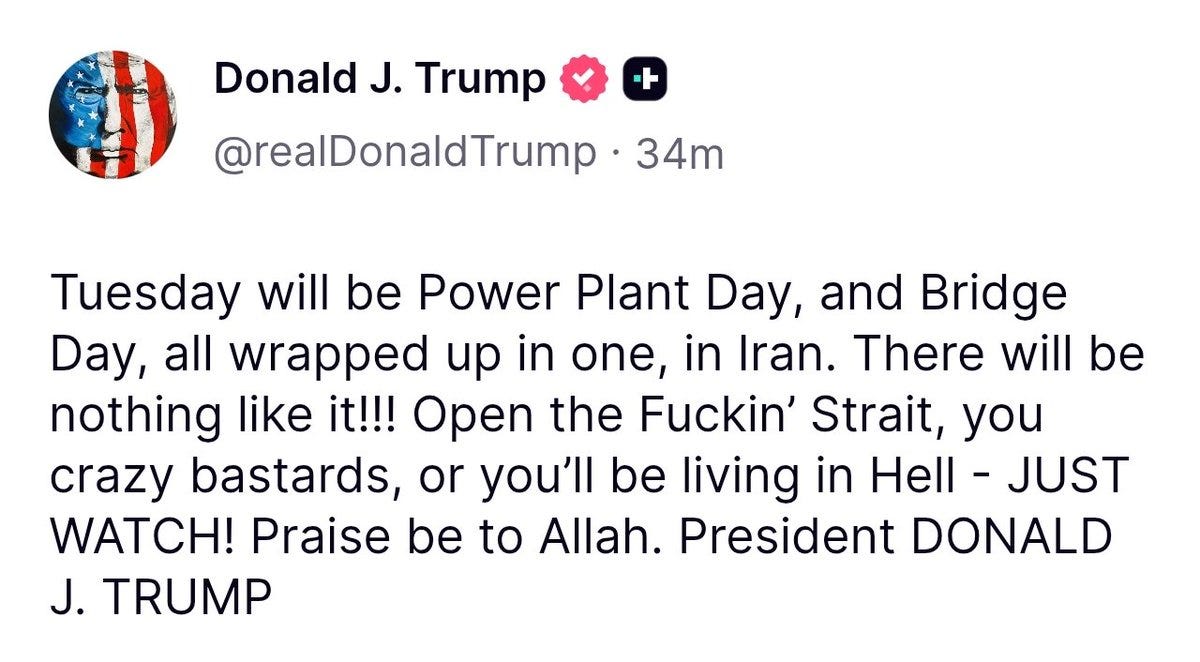

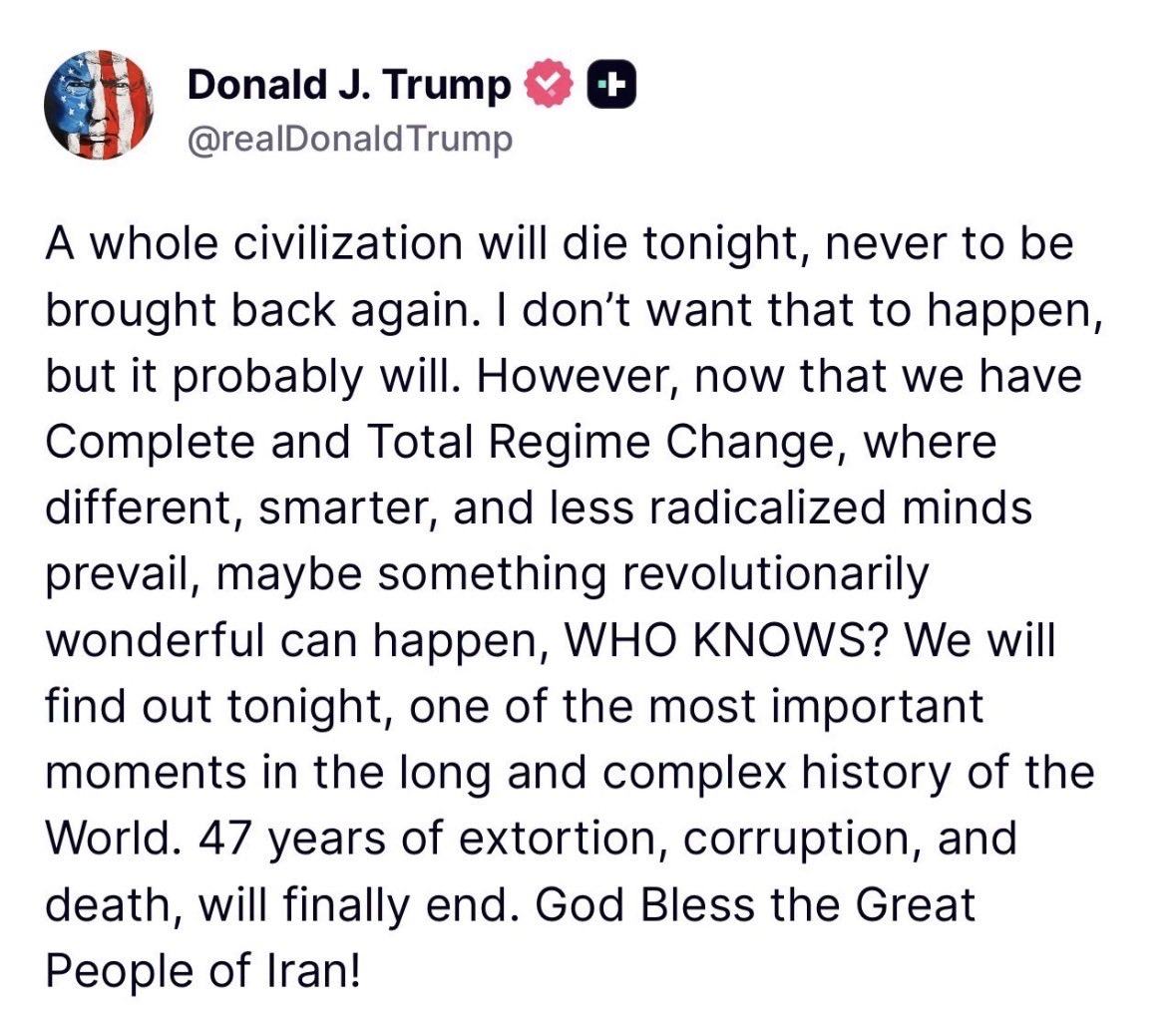

So on Easter Sunday morning, he reacted with volcanic fury, promising to destroy all of Iran's civilian infrastructure unless the strait were reopened. He then followed it up on Tuesday morning with an even more outrageous threat to annihilate all of Iranian civilization.

But the Iranians remained steadfast and merely released another one of their popular LEGO animations, carrying their warning that if their civilian and energy infrastructure were destroyed, they would retaliate by inflicting the same consequences upon America's Gulf Arab allies. The entire region's natural resources would be lost for many years, producing an unimaginable global economic catastrophe.

How to defeat a hegemon

Meanwhile, Trump's wild, bloodthirsty threats against civilian targets led to waves of criticism by many of his staunchest former supporters such as Tucker Carlson, Marjorie Taylor Greene, and Alex Jones. They denounced him as a blasphemous non-Christian and "an evil psychopath," and large numbers of even his own Truth Social followers turned against him.

Subscribe to New Columns

Trump recognized that following through with his threats would be a terrible mistake, so he desperately sought some plausible excuse to call off the attack without appearing to back down. The Iranians had already presented a 10-point set of demands, and Trump suddenly now seized upon it, saying he accepted it as the basis for peace negotiations. The Wall Street Journal reported this and published the text released by the Iranians:

In announcing a cease-fire with Iran, President Trump said Tuesday the U.S. had received a 10-point plan that was a "workable basis on which to negotiate."On Wednesday, Iranian state media released what Iran said that proposal was—a list that appeared to reflect many of the nation's longstanding demands.

As Prof. John Mearsheimer noted at the time, Trump's public acceptance of Iran's maximalist demands amounted to an American surrender:

After two previous rounds of negotiations had been interrupted by deadly, surprise American attacks, the Iranians had repeatedly refused to hold any future meetings with America and rejected any temporary cease-fire. But with America now apparently acceding to Iranian terms, they finally agreed to talks in Islamabad. As part of that process, they also accepted a two week cease-fire, but emphasized that they would maintain their severe restrictions on transit through the Strait of Hormuz during this period:

Iran told mediators it would limit the number of ships crossing the Strait of Hormuz to around a dozen a day and charge tolls under the cease-fire struck by President Trump, showing Tehran plans to tighten its grip on the world's most important energy-shipping lane...Four ships were allowed to pass Wednesday, the fewest so far in April, according to S&P Global Market Intelligence, down from more than 100 a day before the war. Iran is requiring ships to work out toll arrangements ahead of time and then pay the fees in cryptocurrency or Chinese yuan, mediators and shipbrokers said.

However, the Islamabad peace negotiations proved a total fiasco, breaking up in complete failure after less than 24 hours.

The Iranians sent a large, experienced team consisting of more than two dozen political officials, diplomats, and technical experts, having full authority to come to an agreement. But the American team was led by Vice President JD Vance and New York City real estate developers Jared Kushner and Steve Witkoff, with both of the latter being fiercely committed partisans of Israel. Moreover, Vance apparently possessed no independent negotiating authority, and during the process he reportedly placed more than a dozen calls to consult with President Trump or Israeli Prime Minister Benjamin Netanyahu on the various issues.

The Iranians had only agreed to hold peace talks because Trump had declared that Iran's own 10-point plan would be the basis for the negotiations. But all of that was now totally forgotten as the Americans merely repeated their own maximalist demands, all of which were utterly unacceptable to the Iranians. So whether intentionally planned or not, the entire process had amounted to little more than a bait-and-switch operation, with the Americans absurdly seeking to win at the negotiating table what their military had completely failed to achieve in six weeks of combat.

Prof. Mohammed Marandi of Tehran University had been a member of the Iranian delegation and in numerous interviews he recounted the very strange nature of the negotiating process and its aftermath.

Among other things, he noted that just a few days earlier, a prominent Washington Post columnist had urged America to assassinate all of Iran's leaders and negotiators if they refused to accept American demands. Given that so many top Iranian officials had already been killed under similar circumstances, Marandi said that he and his colleagues all believed that their plane might be shot down as they returned from the failed talks. The Pakistanis sent more than a half-dozen jet fighters to escort them safely back to Iranian territory, and they then landed close to the border, traveling the rest of the way home on land. In recent centuries, these sorts of concerns about physical safety have surely been much more typical for mafia dons at their summit meetings than during international diplomatic negotiations.

The failure of these peace talks led Trump to announce that he would impose his own blockade on the Persian Gulf, ordering his navy to seize all cargo vessels that passed the Strait of Hormuz in hopes of eliminating Iranian oil revenues. Given the dangers of Iranian missiles, our warships were forced to remain far from the Iranian shore and interdict those vessels on the high seas, constituting blatant acts of illegal piracy. Just the previous month, severe concerns over the shortage of global oil supplies had led the Trump Administration to lift all sanctions on Iranian sales, but they now completely reversed that policy, further demonstrating their flailing incoherence.

Since 90% of Iranian oil was sold to China, seizing China-bound oil tankers in international waters effectively amounted to imposing an illegal oil blockade against that country, an obvious act of war.

Furthermore, as the Wall Street Journal soon explained, such blockading actions against both Iran and China would be almost completely ineffective as a means of exerting pressure:

Iran has built a stockpile of oil outside the Strait of Hormuz that could help it—and Chinese crude importers—withstand a blockade for weeks or even months...This leaves Iran with around 160 million barrels of oil already loaded onto ships floating on the ocean outside the Persian Gulf today. Some of the crude is already spoken for and on its way to Chinese buyers. But in theory, Tehran can keep its customers supplied until mid-July, based on the 1.8 million barrels a day of Iranian oil that China imports.

President Trump hopes that choking off oil revenues will force Iran to the negotiating table. Tehran is betting it can withstand the disruption longer than the global economy. Based on its oil stockpile at sea, that is more than mere bluster.

At this stage, I was working on my new article and matters seemed to have resolved themselves quite clearly in my own mind.

Although the dust hadn't yet fully settled, it seemed obvious to me that Iran had won the war with America, with Trump's only remaining escalatory option being the nuclear or non-nuclear destruction of Iran. But even if such an extreme step could be successful, it would inevitably lead to the retaliatory destruction of the Gulf Arab states. The resulting long-term elimination of Persian Gulf oil and energy resources that would produce a global catastrophe.

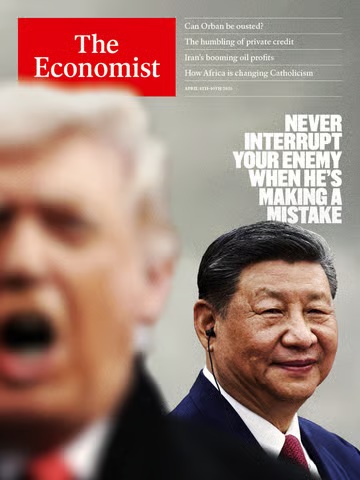

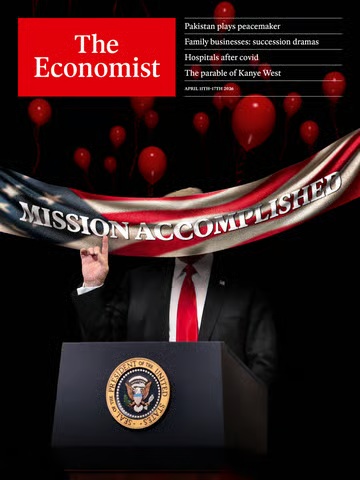

The Economist is one of the world's most influential publications. Although intensely hostile to Iran, several weeks earlier they'd declared that Iran was clearly winning the war, pointing to the Iranian stranglehold over the global economy as the main factor, with their cover showing that stylized image. Two subsequent issues had reinforced that same conclusion, emphasizing that the Iran War was ending in Trump's total defeat and humiliation.

The financial markets admittedly seemed to be living in a parallel universe, operating on the bizarre assumption that the Iranians would very soon reopen the Strait of Hormuz to all cargo traffic and that the war would quickly come to an end. But that merely demonstrated their irrationality or perhaps their deliberate manipulation, and I planned to emphasize those points in the article that I was already preparing.

However wars are often filled with unexpected twists and turns. Early Friday morning, I was shocked to discover that the markets had apparently been correct all along, as Iran's foreign minister Tweeted out that an announcement of what seemed to be exactly such a complete, unconditional reopening:

Trump naturally promoted that huge Iranian concession in several of his own posts, crowing about this outcome that he'd previously spent weeks trying to achieve, and his White House team Tweeted out those messages.

Trump, being Trump, naturally piled on to this victory celebration. He boasted that a final agreement with the Iranians had almost been completed and that he would still maintain his own naval blockade of Iranian oil shipments until everything was finished. According to him, the Iranians had also agreed to give America all their existing enriched uranium, and that although this deal had nothing to do with the cease-fire in Lebanon, he'd prohibited the Israelis from any further bombing.

A very useful piece by former CIA analyst Larry Johnson summarized all the many bold claims that Trump subsequently posted on his Truth Social website:

- The "Hormuz Strait situation is over" and Iran has agreed to never close the Strait of Hormuz again. He described it as "completely open and ready for business and full passage."

- Iran (with US help) is removing the mines it laid in the strait last month.

- Iran has agreed to nearly all (or "virtually all") of his demands, including ending its nuclear program "forever."

- The war is "very close to over" / "close to being over," and a final deal should be completed "very quickly" (possibly with talks this weekend). He said most points have already been negotiated.

- He agreed to a two-week double-sided ceasefire (suspended bombing/attacks) after requests from Pakistani leaders, conditional on Iran fully opening the strait. Despite Iran's announcement that the strait is open, the US naval blockade of Iranian ports will remain in full force until the overall transaction/deal with Iran is "100% complete."

- China's President Xi Jinping is "very happy" that the strait is open/rapidly opening. Trump claimed he is doing this "for them, also — and the World," and that this situation "will never happen again."

- China has agreed not to send weapons to Iran. Trump predicted his upcoming trip to China will be "special" and "potentially Historic," and that President Xi will give him a "big, fat, hug."

- He dismissed NATO as a "Paper Tiger" that was "useless when needed." After the strait reopened, NATO reportedly offered help, but Trump told them to stay away unless they just wanted to "load up their ships with oil."

- He emphasized that the US has already met and exceeded its military objectives. He claimed Iran now has a "new regime" that is "much less radicalized and far more intelligent" than before, making a long-term peace agreement possible. He reiterated that the U.S. will work with Iran "at a leisurely pace" on finalizing the deal.

I found all of these developments absolutely stunning.

Trump was so wild and unreliable in his public statements that I generally disregarded anything he said. But the Iranians had announced the reopening, so perhaps Trump's other claims were also correct. It almost seemed like the Iranians had completely surrendered, though I couldn't understand why.

In all his recent interviews, Prof. Mearsheimer emphasized that as long as the Persian Gulf remained closed, the Iranian bargaining position grew stronger every week, so Iran would be very foolish to settle on any compromise terms.

Since the first days of the war, I'd been arguing that it would be totally impossible for American military forces to reopen the waterway. Our ships would be sunk in any naval assault, while attacking with the many thousands of ground troops we'd brought to the region would achieve nothing except heavy American casualties and probably many POWs. But Iran had now apparently reopened the strait without a single shot having been fired.

I was hardly the only observer entirely taken by surprise. Lt. Col. Daniel Davis is an independent military analyst whose podcast I regularly watch. Just the previous day he had confidently explained that there was only a 1% chance that the Iranians would be willing to reopen the strait without enormous American concessions. But this was soon followed by his breaking-news video declaring that the Iranians had suddenly done exactly that.

Similarly, former Larry Johnson had just published a piece explaining that the latest announcement by Treasury Secretary Scott Bessent of a further round of American economic sanctions against Iran and China had completely closed the door to any peace deal. But this suddenly seemed obviated by Iran's surprising announcement.

The financial and commodity markets naturally responded with massive shifts. The price of oil on the futures market dropped by a full 10%, and American stock prices rose in similar fashion, setting new record highs. So apparently the traders believed that President Donald Trump had finally made good on his promise to bend the Iranians to his will, forcing them to reopen the Strait of Hormuz and perhaps also make all the other major political concessions that he had been demanding.

Admittedly, the initial Iranian statement had been that they were only reopening the strait to commercial vessels for the period of the cease-fire, but once they had made such a huge concession others were likely to follow.

So if they Iranians were now completely relaxing that grip, the war might soon be over on Trump's terms.

Despite the massive bombing campaign they had suffered, just a couple of weeks earlier the Iranians had been unwilling to even meet Americans for negotiations, and now they suddenly seemed close to capitulation, an extremely strange development.

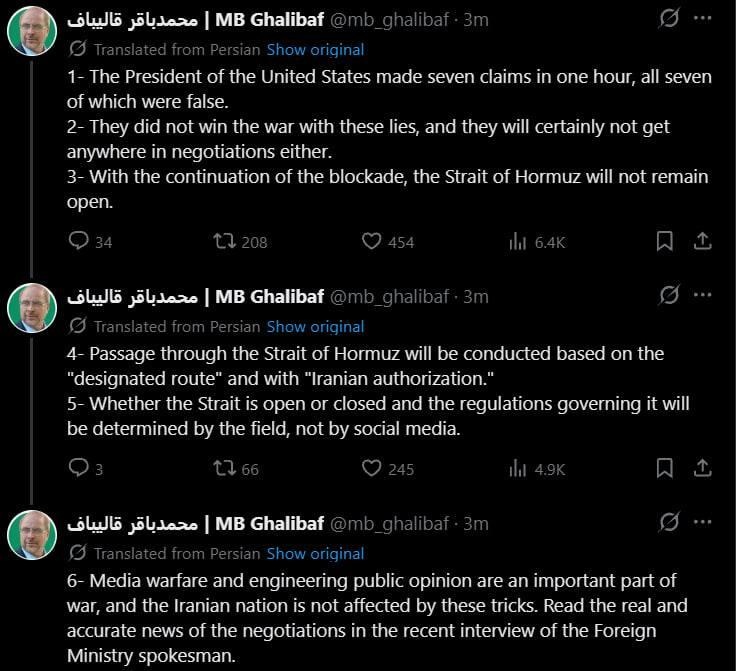

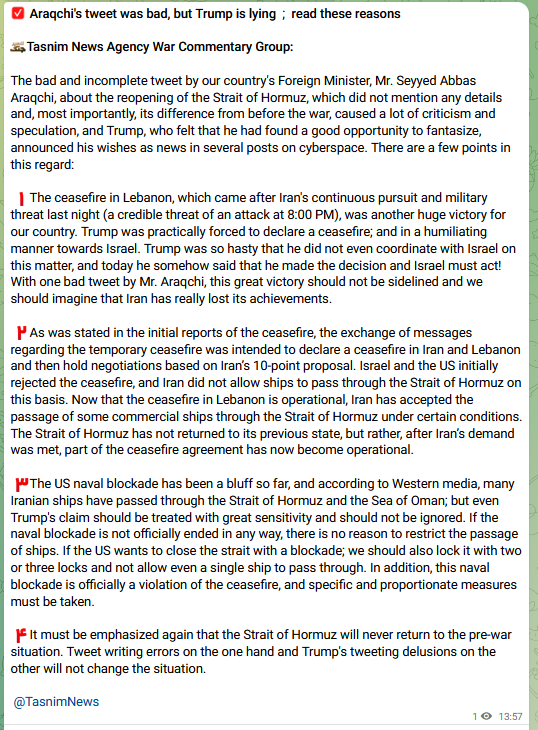

However, no sooner had the world begun digesting that surprising announcement than the Iranians began sharply backing away from it.

The Iranian speaker of parliament soon released a series of Tweets declaring that almost all of Trump's statements were false and that Iran had not changed any of its positions.

Later that same day, Iran's Tansim state news agency released several items and a long statement explaining that the original Tweet declaring the strait reopened had been incomplete and mistaken, and totally misinterpreted by Trump:

The Iranian IRGC declared that the strait was once again closed, and underscored that declaration by firing on a couple of ships that had attempted to transit the waterway.

So any apparent Iranian decision to reopen the Strait of Hormuz had only lasted for less than 24 hours, and matters were back to what they had been.

In many respects, this episode illustrated the awesome power of the Western mainstream media to create its own reality.

A single Tweet by an Iranian official, perhaps unauthorized or poorly phrased and quickly contradicted by other Iranian sources, had suddenly transformed into the world's top news story, boosting stock prices by many hundreds of billions of dollars and drastically cutting the market price of oil. Even following the retraction, all of this probably had a strategic impact, strengthening the determination of Trump and his officials to continue the war rather than to seek some excuse to abandon it.

Meanwhile, other interesting recent developments have probably received far less attention that they warranted.

A few days ago, the WSJ published a highly illuminating front-page article on our military establishment. Running nearly 3,000 words and sharing three co-authors, it bore the provocative title "A Private Equity Billionaire Mounts His Biggest Takeover Yet: the Pentagon."

The piece was a profile of Steve Feinberg, the notoriously secretive private-equity billionaire in question, whom Trump had installed as the No. 2 Pentagon official under Pete Hegseth, our self-styled "Secretary of War."

Hegseth himself is a heavily tattooed drunken rapist, whose outrageous public statements and actions monopolize media attention, thereby allowing Feinberg, his nominal subordinate, to operate in the shadows as he has always preferred.

As the Journal reported, Feinberg originally got his start under "Junk Bond King" Michael Milken, who was later sentenced to ten years in prison and fined $600 million dollars for financial fraud. Feinberg then founded Cerberus Capital Management, which subsequently became the basis of his personal wealth.

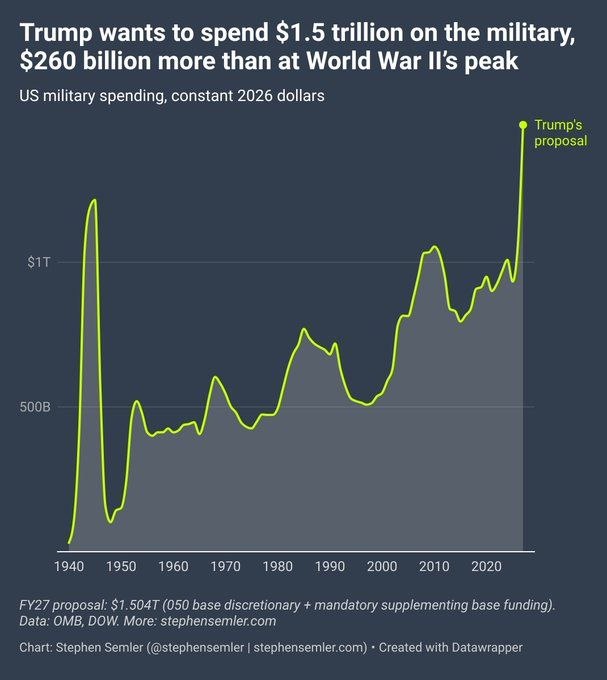

Soon after his appointment, Feinberg persuaded Trump to boost our Pentagon budget a whopping 50% to $1.5 trillion per year. Not only was that figure roughly equal to the total military spending of every other nation on earth, but it was even far higher in inflation-adjusted terms than what we had spent at the height of World War II.

Subscribe to New Columns

The Journal explained that Feinberg has focused on managing that colossal tidal wave of government money, bringing in some of his top Cerberus Capital subordinates to assist him in that difficult task:

Feinberg has surrounded himself with a close-knit circle of advisers with Cerberus ties. The group includes former Cerberus Managing Director John Gallagher and a deal team called the Economic Defense Unit led by Cerberus alumnus George Kollitides.The finance experts negotiate Pentagon contracts with defense companies, according to Michael Cadenazzi, an assistant secretary of defense. "They're the ones structuring the deals to make sure that they work," Cadenazzi said at a Hudson Institute event in February. Some industry executives have nicknamed the squad "Deal Team 6."

"This is a Cerberus takeover," said Steve Blank, an adjunct Stanford professor of entrepreneurship and national security. "Private equity has just acquired its largest organization."

Over the decades, Cerberus has owned a number of military contractors and Feinberg promised to comply with the government regulations requiring that he divest himself of his holdings:

When he joined the government last year, Feinberg committed to transfer his Cerberus holdings to trusts that benefit his adult children. Asked about potential conflicts of interest, Pentagon spokesman Parnell said, "The Deputy is a man of integrity who has conducted himself ethically throughout his entire career."

In recent years, our annual military spending has been more than one hundred times greater than that of Iran, but in many respects we have been getting the worst of the current conflict. So one possible response to this problem would be this massive further increase in such spending.

But an interesting recent article in the New York Times explained that during this current war, we have often expended interceptor missiles costing up to $8 million to shoot down $30,000 Iranian drones. That disparity in cost-effectiveness has helped to explain why our far greater military spending has been much less decisive than might naively be expected.