June 2, 2026

Our Financial Markets and Their Many Irrationalities

I launched my American Pravda series a decade ago next month. My conscious strategy was quite unusual, being almost exactly the opposite of that followed by nearly everyone else covering those same controversial topics.

As some of them explicitly told me, they had always deliberately avoided exploring too many different and unrelated historical controversies. Instead, they believed that they were on safer ground by confining their work to a relatively narrow slice of these.

So some of them spent years challenging the official narrative on World War II or the JFK Assassination or the 9/11 Attacks or took other positions denigrated as "conspiracy theories" by our political and media establishments. But they usually focused on just one or two of those major issues, and ignored the others.

I decided to take the opposite approach and cover as many of those as possible. After years of effort, my American Pravda series has now done this, constituting a broader collection of such material than anything else I've encountered on the Internet.

- The American Pravda Series

- Ron Unz • The Unz Review • 146 Articles • 1,230,000 Words

In an October 2016 article, I'd sketched out the reasoning behind my contrary approach:

Individuals who challenge the prevailing media narrative with unorthodox ideas are often reluctant to raise too many such controversial claims simultaneously lest they be ridiculed as "crazy," with all their views summarily dismissed.

In most cases, this may be the correct strategy to pursue, but if handled properly, an exact opposite approach might sometimes be quite effective...Or as suggested in a quote widely misattributed to Stalin, "Quantity has a quality all its own."

Suppose it is established that there is a reasonable likelihood that the media completely missed and ignored an important matter that should have been investigated and reported. The impact is not necessarily substantial, and many individuals stubbornly wedded to a belief in their establishment media narratives might even resist admitting the possibility that the media had seriously erred in that particular situation.

However, suppose instead that several dozen such separate examples could be established, each strongly suggesting a serious error or omission on the part of the media. At that point, ideological defenses would crumble and nearly everyone would quietly acknowledge that many, perhaps even most, of the accusations were probably true, producing an enormous credibility gap for the mainstream media. The credibility defenses of the media would have been saturated and overcome...

For example, in the original 2013 American Pravda article I raised over half a dozen enormous media lapses, all of them now universally acknowledged: Enron's collapse, the Iraq War WMDs, the Madoff Swindle, the Cold War spies, and various others. Having thereby set the stage by presenting this admitted pattern of major failure, demonstrating that a considerable suspension of disbelief was warranted, I then extended the discussion to three or four important additional examples, none of them yet acknowledged, but all of them perfectly plausible. Perhaps as a consequence, the article received reasonably good attention including by elements of the mainstream media itself, who are often willing to acknowledge the errors of their class so long as these are presented persuasively and in a responsible manner.

- American Pravda: Breaching the Media Barrier

- Ron Unz • The Unz Review • October 24, 2016 • 2,500 Words

This same sort of reasoning also applies to financial matters.

If our markets seem to be severely mispricing one enormous risk, there is a natural tendency to dismiss that possibility. But if there appear to be several such looming financial disasters, all of which have been completely ignored by most traders and investors, faith in the wisdom of these latter market makers begins to dissolve.

This conclusion is further supported by some major examples from the last few decades.

Consider the disastrous Dotcom Bubble of a quarter century ago and the even more disastrous Mortgage Bubble from a few years later. If the markets-and the "smart money" investors who dominated them-were so totally wrong in both those cases, perhaps they might be making similar mistakes today.

Oil Prices Drop As Oil Supplies Approach "Tank Bottom"

Just over three months ago, America and Israel launched their sudden attack on Iran with a surprise decapitating strike followed by a massive wave of bombardments.

Less than 48 hours later I published my first article on the conflict, and although I discussed many elements, I focused on the Strait of Hormuz as the crucial operational theater.

For decades, the Iranians had threatened to close that vital Persian Gulf waterway if they were attacked, and they had done that. So despite all their heavy losses in leadership and military assets, if they managed to keep it closed against American efforts, they could win the war. A quarter century ago, a famous Pentagon simulation exercise had suggested that the Iranians might succeed, but we were about to test that prospect in real life.

Roughly 20% of global oil shipments passed through the Strait, so if it remained closed, there were widespread expectations that world oil prices would quickly skyrocket to $150 or even $200 a barrel, thereby putting tremendous economic pressure on President Donald Trump and his government to end the conflict.

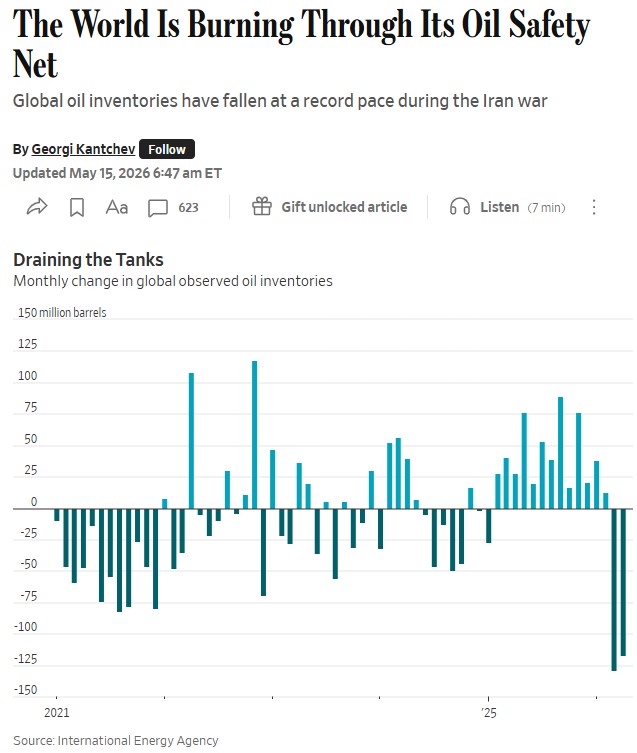

During the weeks that followed, Trump issued endless loud demands that the Iranians reopen the waterway to oil tankers and other cargo vessels, but despite all his bluster, threats, and bombing attacks, the Iranians held firm. The world suffered the largest oil supply-shock in history, far greater than those that had devastated the global economy during the 1970s. Indeed, the Trump Administration was so fearful of the grave economic crisis that they quickly arranged a gigantic release of some 400 million barrels from the West's strategic petroleum reserves, and they also lifted sanctions on the already exported but unsold crude of Russia and even Iran itself.

Yet despite this sudden, massive loss of supply, oil prices only rose a relatively modest amount, nothing at all like the huge spike that almost everyone had predicted.

More than three months later the Strait still remains closed to tanker traffic, but oil prices have recently fallen once again. The August future contracts for Brent crude is now down to just $91 per barrel. This is the lowest level since just a few days after the conflict began when most had expected the war to quickly end, leading to the reopening of the waterway. Furthermore, this price is down some 20% from the peak reached about a month ago, with other oil prices following roughly that same trajectory. So the markets are apparently convinced that the global oil crisis is far less serious than most believe it to be.

Under a properly functioning market economy, commodity shortages soon induce price hikes until a combination of reduction in demand and increase in supply has produced a new equilibrium. But despite the loss of perhaps 14M barrels per day of oil, the resulting price rise has been far too small to have had that necessary impact.

For example, according to an article in the Economist, higher prices have led to increased oil production in Canada, Venezuela, Norway, and Brazil. But all of these countries combined have only raised their exports by less than 1M barrels per day, hardly impacting the huge global shortfall.

There had been widespread claims that the American frackers would quickly boost their output to compensate for any loss of Persian Gulf oil. But an article in the WSJ reported that they had no intention of doing so, with their production only rising by less than 0.03M barrels per day, a totally insignificant account.

These days oil use is highly inelastic, and according to a recent interview with Prof. Steve Hanke , the relatively small increases in oil prices have only reduced global demand by about 2M barrels per day, a figure that I've also seen reported elsewhere.

So due to the minimal rise in global oil prices, the response of market forces to the large and continuing shortfall in Persian Gulf oil has been completely inadequate on both the supply and the demand sides of the equation. As a result, the world seems heading towards what might be called "a very hard landing."

A couple of weeks ago, a major article in the Wall Street Journal emphasized that the existing oil stockpiles that have been cushioning our current shortfall were rapidly being exhausted.

Drawing upon all the figures separately reported in media outlets such as the Journal and the Economist, I had attempted to project when existing stockpiles would be exhausted and the absolute physical shortage of oil would suddenly produce a dramatic spike in prices. I lack expertise in these matters and my estimate of the month of May turned out to be mistaken. But others with far greater knowledge of the industry have continued to issue dire warnings.

On Friday, CNBC reported the alarming remarks of a top oil industry executive:

Exxon Mobil warned Thursday that oil inventories will fall to record low levels in coming weeks, forcing prices to spike and curbing demand.

"We're approaching unheard of inventory levels," said Exxon Senior Vice President Neil Chapman at a conference hosted by Bernstein in New York.

"I mean really, really low levels," Chapman warned. "You can debate whether that's going to hit, those really low levels, in two weeks or three weeks. Once you get to that point, then you'll see price shoot up."

The price of physical Brent oil cargoes will spike to $150 to $160 per barrel when inventories hit all-time lows in coming weeks, the executive said. "When the price gets to a certain level, demand destruction brings it back into balance," he said.

Brent futures for July delivery, the nearest contract, closed under $94 per barrel Thursday as investors once again held out hope for a settlement between the U.S. and Iran that will reopen the Strait of Hormuz.

As that story reported, there appears to be a gigantic gap between July Brent oil futures and projected July Brent oil prices.

I suppose this might be explained by a widespread belief that the Iranians are about to fully reopen the Strait to oil tanker traffic just as Trump has been repeatedly claiming for the last three months. But although I lack any expertise in commodity markets, I do feel extremely skeptical of such a geopolitical development.

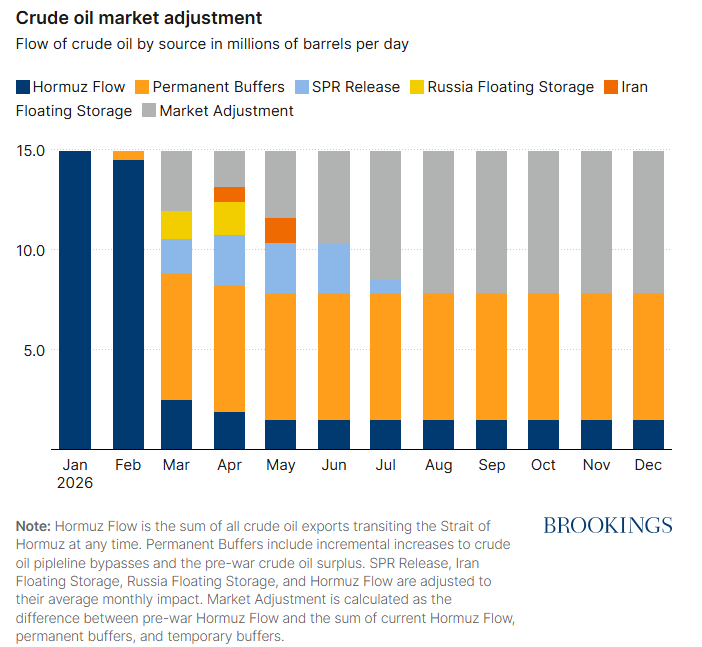

Meanwhile, a few days ago the Brookings Institution published an excellent analysis of the global oil situation entitled "The Timing of the Impending Crude Crisis" that came to some important conclusions. One point of confusion has been the tendency to loosely conflate the supplies of crude and refined products so the researchers decided to simplify the issue by focusing entirely on the former.

Just as I had done, they took into account the loss of Persian Gulf shipments, the releases from strategic petroleum reserves, the de-sanctioned Russian and Iranian oil, and various other factors. Their figures for each of these were somewhat different than the ones I'd sometimes seen mentioned in the media, so their calculations were also different and probably more accurate. They conveniently summarized all of their results in a simple chart.

According to their analysis, existing global stockpiles should be exhausted in July, at which point prices would spike to something like $150 per barrel or more for Brent oil, just as the Exxon executive had suggested.

This timeline also seemed roughly the same as the one sketched out at the beginning of May by commodities expert Jeff Currie, a senior advisor to the Carlyle Group.

"I've never seen anything like it before."

Storage tanks for oil, jet fuel, diesel, gasoline will be running out in Europe in May.

Oil storage tanks in the United States will run empty "somewhere in the July 4 period,"

- Carlyle's Jeff Currie pic.twitter.com/TIsL6rKUWX

- Wall Street Mav (@WallStreetMav) May 6, 2026

This supply scenario might be affected if Iran suddenly reopened the Strait of Hormuz. But that would require a capitulation either by the Iranians or by Trump, neither of which seemed very likely to me. So if we excluded those two possibilities, the current future price of $91 for August Brent oil was just as absurd as I've been saying all along.

One important point was that the Brookings analysis never considered the substantial risk that Trump would choose to restart the war with Iran by attacking that country's infrastructure. The Iranians have repeatedly warned that if that happened, they would respond with massive force, destroying the energy and civilian infrastructure of the Gulf Arab states that had enabled those attacks. Those exchanges would destroy most of the Persian Gulf oil facilities, drastically reducing supplies for years to come. So under that dire scenario, oil prices would surely skyrocket far past the high levels already suggested.

The contrary factor has been the widespread belief that global oil prices would plummet once a peace agreement with Iran led to the reopening of the waterway, and that such an agreement is now close at hand. This has been the regular refrain of Trump Administration officials including National Economic Council Director Kevin Hassett, who emphasized this point in a FoxNews interview about a week ago.

NEC Director Kevin Hassett: "We're already seeing signs that people are a little bit wary about buying oil on the spot market right now because they expect the price to drop a lot sometime soon, so that's a very, very good sign." - Fox pic.twitter.com/rC2KZioEok

- Energy Headline News (@OilHeadlineNews) May 24, 2026

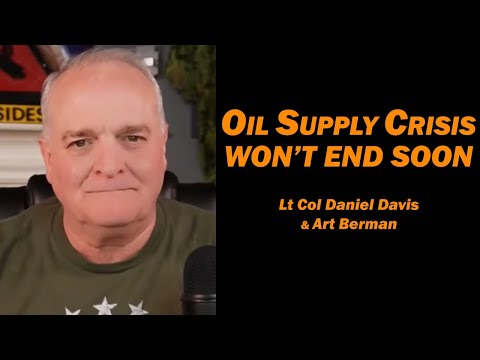

But a few days later an experienced energy consultant named Art Berman was interviewed for an hour, and he debunked and ridiculed that sort of analysis as absurdly naive wishful thinking.

Drawing upon his half-century of work in oil markets, Berman argued that these sorts of statements by Hassett and others demonstrated their total ignorance of the practical details of the oil industry.

Even once the Iranians fully reopened the Strait to traffic, it would probably take several months before the huge number of trapped tankers could exit the Persian Gulf and reach their various global destinations, so the massive shortage of oil supplies that would be hitting the world in July was already baked into the cake. Under the best of circumstances, the severe shortages would continue at least into September, and Berman even believed that tanker traffic would remain less than half of its previous levels for a year or more after any such reopening.

He claimed that all knowledgeable oil industry experts shared his views, and that oil prices of $150 or closer to $200 per barrel seemed almost certain once our existing stockpiles were exhausted in the next few weeks.

According to him, the totally unrealistic oil price futures we have been seeing have been determined by "the dumb money" that seems to believe the statements of Trump and his equally ignorant or dishonest officials.

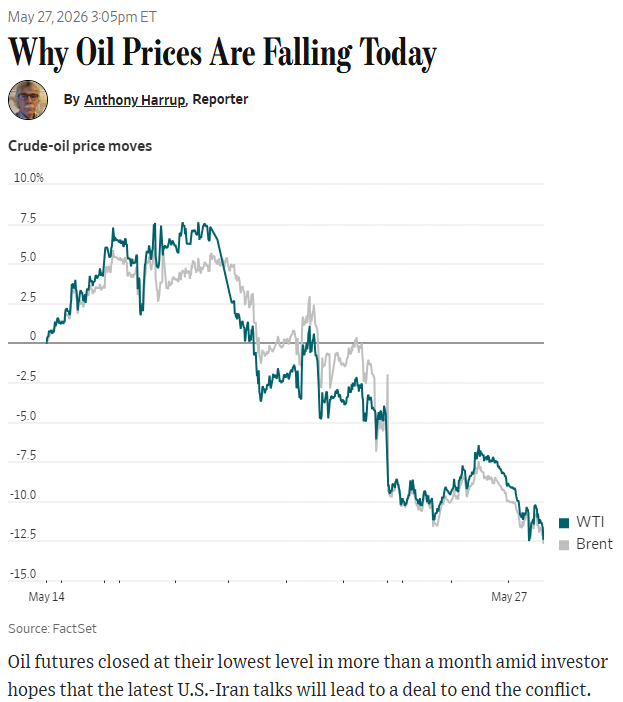

On something like a dozen different occasions, Trump has publicly announced that a peace agreement with Iran had nearly been concluded, and each of those times oil prices have substantially dropped, certainly supporting Berman's claims that these prices are controlled by "dumb money."

A perfect example of this came a few days ago when the Journal reported that the recent sharp drop in oil prices had been due to investor hopes that the latest public statements of the Trump Administration that a peace agreement was about to be signed were more realistic than all of their many previous ones. Instead, the Iranians retaliated for an American attack by hitting our air base in Kuwait with a ballistic missile, but oil prices still stayed down.

Another possibility might be that these seemingly irrational movements in oil prices were explained by the AI systems that apparently control 70% of daily trading on the markets. Perhaps these regularly reacted to Trump's unreliable statements merely based upon their expectations of how all the other AI trading systems would react.

A sharp-eyed observer also noted that the official EIA chart showing the level of America's strategic petroleum reserves had not been updated since the massive drawdowns first began in March. So he wondered whether these powerful AI trading systems might still believe that our oil stockpiles remained far larger than they actually were, thereby helping to explain why market prices for oil have not risen as much as expected.

The Inflated Market Value of Meta/FacebookThe Economist and the Wall Street Journal are two of the world's most highly regarded mainstream publications, especially authoritative on business and financial matters. They have repeatedly published very forceful articles on the disastrous economic consequences of the loss of oil and other vital Persian Gulf commodities due to the continuing closure of the Strait of Hormuz. Yet their warnings seem to have been totally disregarded by the financial markets, which have only modestly raised their oil prices, a very strange and surprising state of affairs.

However, in my first article on the Iran War I had noted that this situation was hardly unique. Other articles in those publications have been equally ignored by Wall Street traders and investors.

A perfect example came earlier this year when an important WSJ analysis argued that most of our Tech giants had been using the dubious accounting techniques of financial engineering to massively inflate their supposed free cashflows. Meta Platforms, the parent company of Facebook, provided the worst example of this.

Meta Platforms looks like a money-printing machine. So why has it been loading up on billions of dollars in debt to pay for its new data centers?

It turns out that the abundant free cash flow that Meta reports to investors is something of an optical illusion. Yes, it generated billions in cash last year, but that was largely devoured by the all-too-real cash costs that come with paying stock-based compensation to employees. Those included billions of dollars in withholding taxes triggered when employee shares vested, and billions more for share buybacks used to offset share dilution from those same awards.

Viewed this way, it's easy to see why Meta more than doubled the debt on its balance sheet last year to $58.7 billion. It borrowed because it had to. And that debt is only the part that is visible. Meta's books don't include the debt from a $27 billion data-center project under construction that Meta kept off its balance sheet through complex financial engineering.

For investors, this raises a vexing valuation issue. At $1.66 trillion, Meta's stock-market value already looks expensive at 38 times reported free cash flow for 2025. The ratio becomes stratospheric, exceeding 1,000 times, if free cash flow included the cash costs tied to stock-based pay...

Free cash flow is an important financial metric. Investors rely on it as a proxy for the discretionary cash a company has left over after reinvesting in its business to reward shareholders or pay down debt.

Yet the term free cash flow has no uniform definition under the accounting rules. It is typically calculated as cash flow from operating activities minus capital expenditures, or capex. And, as Meta's numbers show, it needs a rethink.

Meta reported $43.6 billion of free cash flow for 2025. That was the result of $115.8 billion of operating cash flow minus $72.2 billion of capex. On paper, Meta's core business handily covered its gigantic artificial-intelligence infrastructure build-out.

In reality, cash costs directly tied to employee stock awards consumed $42 billion, or 96%, of Meta's free cash flow last year. A Meta spokesman declined to comment...

"If you really want to get the true valuation of the business, you have to adequately reflect all of the operating costs as operating activities. And the way free cash flow is traditionally calculated does not do that," says Kevin Koharki, an accounting professor at Purdue University. He recommends further adjusting free cash flow to include the cash costs related to stock-based pay. "We can delude ourselves for a while that this is not a real cost, but we're only fooling ourselves at the end of the day," he says.

These accounting tricks were quite reminiscent of those widely employed by the leading Tech companies in the latter stages of the Dotcom Bubble of a quarter century ago, a practice that I'd ridiculed at the time in an op-ed published in the Los Angeles Times.

Subscribe to New Columns

Just a few weeks after the Journal ran that recent column, Meta announced that it was laying off 10% of all its employees, hardly what might be expected from a company that was allegedly so enormously profitable.

Meta's current market value is around $1.5 trillion, and if that contrary financial analysis were correct, that figure should be reduced by 96%, puncturing the valuation bubble produced by misleading accounting. Although Meta was the most extreme example cited by the Journal, similar accounting problems existed in the cases of the other multi-trillion-dollar Tech giants such as Alphabet, Microsoft, and Nvidia.

In further support of Meta's weakness, we should consider some of the disastrous business decisions previously made by its longstanding CEO Mark Zuckerberg. For twenty years Facebook has been the money-printing engine of his corporation, but a few years ago Zuckerberg became so enthralled by the supposedly tremendous possibilities of the so-called "Metaverse" that he made it the central focus of his future business plans, even renaming his corporate parent entity "Meta Platforms."

Unfortunately for him, the Metaverse never generated any significant public interest or revenue. So after having lost some $80 billion in the failed project, he abandoned it, with only the corporate name surviving as its lasting legacy.

Consider the possibility that the Journal's financial analysis is correct and that a more realistic market value for Meta should be something 96% below its current figure or perhaps around $60 billion. Under such an analysis, that squandered past investment of $80 billion looms very large.

When that shocking Journal article ran in February and the Meta spokesmen refused to dispute its financial analysis, I naturally expected to see a sharp drop in the stock price of a company whose true market value was arguably 96% lower what it was believed to be. Yet after various ups and downs, its current price is today almost exactly what it was on that date.

My only possible conclusion is that few if any traders or investors read the Wall Street Journal or pay any attention to its articles.

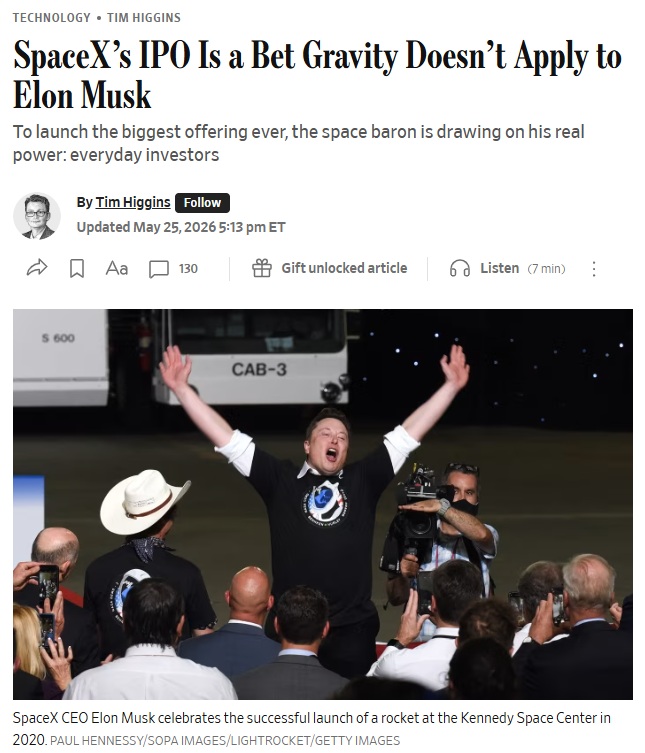

Elon Musk and His SpaceX IPOFor many years, Zuckerberg had probably been the highest-profile Tech CEO, but during the 2020s he was dethroned by Tesla CEO Elon Musk. The latter's trail-blazing EV company captured the imagination of the world, while becoming roughly as valuable as every other auto company combined. Musk's other company SpaceX is now on the verge of going public, at an expected market value of perhaps $1.5 trillion or more, representing the largest IPO in our national history.

Musk had founded SpaceX in 2002, and after many years of losses—and numerous brushes with bankruptcy—he successfully made it the world's overwhelmingly dominant launch provider. His very innovative use of recoverable booster stages drastically reduced the cost per kilogram of getting items into low earth orbit.

Amazon founder Jeff Bezos had also established his own private space technology company Blue Origin a couple of years earlier, but it largely stagnated over time and completely fell behind its plucky Musk rival despite its owner's vastly greater financial resources. Bezos has more recently made a major effort to catch up, but his latest rocket suffered a massive explosion a few days ago, destroying the 48 Amazon satellites it was carrying as well as the launchpad. This probably set the company back at least many months and will almost certainly cause it to miss its FCC deadline for deployment. This mishap demonstrated that space travel was far from easy and underscored the magnitude of Musk's achievement.

Meanwhile, over the years Musk's Starlink satellite division had become sufficiently profitable to move his entire company into the black.

But Musk is a notorious financial daredevil, and apparently running a newly profitable company was not to his taste. So in the months leading up to his planned IPO, he merged the now-profitable SpaceX with xAI, another of his companies, itself created by the merger of his new AI start-up with X, the renamed version of social media giant Twitter. The vast capital expenditures necessary for AI development have now restored the combined entity to its usual state of massive annual financial losses as far as the eye can see, and indeed those tremendous capital requirements were apparently a major reason for the IPO.

Despite these large projected losses, Musk's IPO seems likely to draw huge support from his fervent fan-base of retail investors.

However, major media outlets and the experts they consulted have turned a far more skeptical eye. For example, a few days ago, the Journal published a column appropriately entitled "SpaceX's IPO Is a Bet Gravity Doesn't Apply to Elon Musk".

The piece opened with the following paragraphs:

The SpaceX IPO filing is full of so many red flags that it would have scuttled other launches.

But the laws of gravity don't apply here, in part because of years of work by Elon Musk to build his business empire with the eager assistance of everyday investors. He's tapped into a collective social-media psyche that runs on vibes and enthusiasm and hope for a better future that he has become so masterful at selling.

His sales pitch has gained credibility with the success of Tesla, where he is also CEO, and SpaceX, which has reinvented the space industry and became the top launcher of satellites in the world. Its Starlink business, which is a big driver of revenue, has extended internet connectivity globally and helped to extend Musk's geopolitical clout while also helping make him the world's richest man.

And in launching what is likely to be the biggest IPO ever, Musk is yet again leaning in to a message of hope.

"Our mission is to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars," the company wrote in filings made public this past week.

That phrase—"light of consciousness"—was mentioned almost a dozen times throughout the prospectus. There was also an artist's rendering of life on Mars that could easily have been a scene from the current season of Apple TV's sci-fi drama "For All Mankind." And the dense paperwork included an out-of-this-world projected total addressable market for SpaceX at $28.5 trillion, just a few trillion dollars shy of the entire U.S. gross domestic product.

If it wasn't clear enough, the filing noted: "We believe that space represents the largest economic frontier in human history."

Then there were troublesome bits. More than $1 billion in related transactions between Musk companies, including $131 million of Cybertrucks purchased by SpaceX. The amount of red ink surprised some—a situation made worse by Musk's decision to buy another one of his startups, xAI. The merged companies—a rocket maker/satellite company/AI lab—had a loss of almost $5 billion last year on $19 billion of revenue.

So the company is expected to be valued at something approaching 100 times its annual revenue of $19 billion, despite losing $5 billion per year, quite remarkable financials for a record-setting IPO.

A day later, the New York Times published an article highlighting some of the disturbing corporate governance aspects of SpaceX:

In January, SpaceX granted Elon Musk, its founder and chief executive, a pay package that eventually totaled 1.3 billion restricted shares. The award was contingent on the rocket company's establishing a colony on Mars with one million inhabitants and launching high-powered data centers into space.

Mr. Musk has not achieved those goals. Even so, he can vote those 1.3 billion shares in shareholder decisions, according to SpaceX's offering prospectus, which was released on Wednesday. In other words, the company is allowing Mr. Musk to vote with shares he has not yet earned.

"I have never heard of this," said Ann Lipton, a law professor at the University of Colorado, Boulder. "He basically found a way to hack the normal rules of corporate organization."

The restricted shares weren't the only unusual corporate governance arrangement that SpaceX revealed as it prepares what could be the largest initial public offering ever. The company, which builds rockets and operates the Starlink satellite internet service, has valued itself at more than $1.25 trillion, and its I.P.O. — which is set to happen as soon as next month — is likely to create a bonanza for Wall Street, Silicon Valley and, of course, Mr. Musk.

Among the atypical arrangements, SpaceX does not plan to have the majority of its board be independent directors. It added that it would not use a committee of independent board members to determine executive compensation, as most companies do. And its governing documents say any shareholder claims under federal securities law must be resolved through arbitration.

All of these moves appear to benefit one person: Mr. Musk.

The measures give him more command over a company where he controls 85 percent of shareholder votes, corporate governance experts said. They allow Mr. Musk to put more insiders onto SpaceX's board, pick the people who determine his pay and largely insulate himself from shareholder lawsuits, they said.

The measures are "a defensive moat" that will "entrench him permanently" as chief executive, said Brian Quinn, a law professor at Boston College who studies corporate governance. He called the January compensation package "insane"...

SpaceX's governance measures serve as a warning to those looking to buy into its I.P.O., Mr. Quinn said. "It's terrible for shareholders," he said.

Mr. Musk, SpaceX and Tesla did not respond to requests for comment...

The shares give Mr. Musk the power to decide many company matters on his own. "Mr. Musk will have the power to control the outcome of matters requiring shareholder approval, including election of all our directors, and to control our business and affairs," according to SpaceX's prospectus...

Some of SpaceX's governance measures have already drawn scrutiny. This month, leaders overseeing state and city pension funds in New York and California criticized the company's stipulation that shareholder challenges must be resolved through mandatory arbitration.

"Mandatory arbitration eliminates the class-action lawsuit structure essential to remedying widespread harms," officials overseeing the pension funds wrote in a letter to SpaceX. They added that no major U.S. issuer had ever had such a provision for its I.P.O.

SpaceX's corporate governance structure "freaks me out," Ms. Lipton of the University of Colorado said.

Although other technology or media companies are also controlled by the super-voting shares of their founders, such control has always been somewhat mitigated by the possibility of investor lawsuits. But as Lipton emphasized in a Journal article a few days earlier, a combination of legal factors has essentially blocked that possibility for SpaceX, thereby essentially eliminating any future influence of shareholders at the trillion-dollar company that they nominally owned:

In the case of SpaceX, there are restrictions that could make it virtually impossible for most shareholders to sue the company. The first is a provision allowed under the state law of Texas, where SpaceX is legally based, that prevents lawsuits from shareholders collectively representing less than 3% of the stock issued. The second is an arbitration requirement that restricts investors from banding together to file class-action suits.

"They're essentially closing off every possible avenue for shareholders to have any influence at all," said Ann Lipton, a law professor at the University of Colorado, Boulder.

Certainly Musk has had an outstanding track record in the innovative industrial companies that he has established and run. Perhaps he will use the funds the investors are providing him to successfully establish a human colony on Mars or achieve some other such noteworthy results. Or perhaps he will use the money for something entirely different.

But in any event, none of those investors who actually owned his company and contributed those funds will have any say whatsoever on the matter, and that includes all the passive shareholders whose market index funds will soon automatically include a significant slice of SpaceX shares.

Indeed, just a couple of days ago CNBC reported that Musk had announced a dramatic change in one of the largest financial agreements of his company, totally contradicting what he had previously declared in the official 300-plus page IPO offering circular.

In the famous South Sea Bubble of the 18th century, a slightly embellished story of the offering circular of one of the companies that went public in 1720 described it as "a company for carrying out an undertaking of great advantage, but nobody to know what it is." To some extent that seems an apt description of what will be the largest IPO in American history.

The Amazing Technology of AIEarlier this year, Musk merged his successful launch and satellite company founded in 2002 with his new cash-burning xAI startup. In doing so, he presented a surprising vision of how these seemingly unrelated enterprises fit snugly together.

Although Musk was apparently dead serious, his April Fools' Day filing with the SEC declared that he intended to launch one million solar-powered data-center satellites into space, thereby providing his AI division with computing resources that would totally dwarf any of its terrestrially-bound competitors.

Similarly, Mark Zuckerberg justified his massive recent layoffs of employees by his need to reallocate so much of his available corporate resources to AI development. Over the last couple of years, his AI project has become the central goal of his technology efforts.

One major reason that the global supply shock from the Iran War has not had any noticeable impact upon stock prices has been that it has been swamped by the enormous rise of AI-related Tech stocks. That entire boom had been set off less than four years ago when OpenAI released its ChatGPT in November 2022, with that free chatbot attracting some 100 million regular users within a couple of months, a faster rate of growth than almost any other technology in world history.

Being preoccupied with other things, I personally paid little attention to the product at the time and wasn't sure how seriously to take the reports of its amazing capabilities that I read about in my regular newspapers. But I eventually found that the technology was as remarkable as the media pundits had claimed.

However since these chatbots were supposedly trained upon hundreds of billions of words of text scraped off the Internet, I didn't see that it had much relevance to our own website, whose total content was so tiny by comparison.

But I soon discovered that I'd been mistaken about all of this. Apparently, although generic AI systems must first be trained upon enormous quantities of text, once that training has been completed they can then be "focused" upon a much smaller body of content, which they will then treat as their primary source of knowledge, drawing upon it for any questions that they were asked.

My own writings totaled a couple of million words, which was apparently more than enough for that purpose, and someone tested it in that way. The results were quite amazing to me, with the chatbot very effectively responding to queries by using information drawn from my own work. So apparently it was easy to produce a simple chatbot that reasonably reflected my own perspective and accumulated knowledge.

I therefore had all my writings fed into a ChatGPT4o system that produced a customized Ron Unz Chatbot, and made it available on the website, doing the same for many of our other writers whose total content was sufficiently large. I explained these new capabilities in a couple of articles I published almost two years ago:

- American Pravda: Laminated Mouse-Brains and the Magic of AI

- Ron Unz • The Unz Review • June 10, 2024 • 15,000 Words

- Questioning Our Writers, Whether Living or Dead

- Ron Unz • The Unz Review • June 15, 2024 • 6,600 Words

As those articles showed, these customized chatbots responded to questions about historical events in ways that were dramatically different than the responses of the generic ChatGPT chatbot, and I attached these customized chatbots at the bottom of all the articles by those particular authors.

But as I further tested these systems, I developed some misgivings.

For example, the Ron Unz Chatbot usually did respond to controversial historical questions with answers reflecting my own views, but on other questions it often sharply deviated from these. So I was concerned that it might give users a mistaken impression of my own beliefs.

The problem was even more serious for many of the other customized chatbots, which had been focused upon much smaller bodies of writing.

So although I kept these systems in place, I made little effort to promote or highlight them.

Then early last year, I added a much simpler AI feature to the website. Many of the articles we publish are quite long, including my own, and people had often suggested that it would be nice to have simple summaries available.

Therefore, I used ChatGPT to automatically provide short text and outline summaries of all website articles longer than 1,000 words, with all of that available through an "AI Summary" button near the top:

- Providing AI Summaries of Website Articles

- Ron Unz • The Unz Review • February 14, 2025 • 2,400 Words

But my most important use of AI came about a year ago when I discovered that it could produce extremely detailed and thorough fact-checking runs for long, complex articles, including for those on the highly controversial historical topics in which I specialized.

When I'd tried fact-checking runs using ordinary chatbots, the results were so mediocre as to be useless. The AI system more or less assumed that the standard narratives provided in sources such as Wikipedia were entirely correct and declared that any contrary claims were false.

But as I explained a year ago, some advanced AI models operated at a much more sophisticated level:

...I recently learned that OpenAI had released a new and especially powerful version of ChatGPT called Deep Research.

Whereas ChatGPT and most other chatbots are designed to respond within seconds, the Deep Research AI may spend up to 30 minutes working on a given assigned topic, but it uses that time to produce remarkably advanced results. For example, on a standard benchmark test, the GPT-4o system scored only 3.3%, DeepSeek's R1 model did much better at 9.4%, but Deep Research rated a vastly superior 26.6%.

Once I began testing the Deep Research AI, these numbers seemed quite plausible to me. I discovered that the system can very effectively be used to fact-check long, complex articles of the sort that I often write. After a couple of such tests, I was so impressed that I have now had dozens of my American Pravda articles fact-checked by Deep Research...

I was absolutely astonished by the analytical quality of what Deep Research produced, results that fully validated the dramatic claims made in media accounts.

It's been widely recognized that all of these recent AI systems have easily blown past the decades-old "Turing Test" of machine intelligence, but the output of the Deep Research AI was entirely on a different level. Many or most of its full-power analysis runs seemed as if they had been written by an exceptionally intelligent individual who had read nearly everything published on the entire Internet and also had almost total recall.

Although I'm still not entirely convinced that the hundreds of billions of dollars currently being invested in AI will ever produce an adequate financial return, the AI systems created are certainly one of the most amazing things I've ever encountered, being closer to magic than software technology, and doing things I never would have believed possible in a million years. If some company had invented a practical teleportation device, I probably would have regarded such a product as much less remarkable.

- Fact-Checking American Pravda

- Ron Unz • The Unz Review • May 26, 2025 • 8,600 Words

When operating in full-power mode, the quality of these Deep Research runs was stunning. They might take an hour or two to run, failing perhaps a quarter of the time, and they very occasionally contained errors or hallucinations. On a few especially "touchy" topics, they seemed to have been heavily indoctrinated to maintain official orthodoxy. But these were minor blemishes on what amounted to a magical genie.

The $200 OpenAI plan allowed 125 of these full-power runs per month and I spent the next few months producing these very detailed fact-checking runs for all the many hundreds of articles I'd published since the early 1990s. Each of these is now available at the "AI Fact Check" button found just below the title, and I published a few articles summarizing some of these impressive results, including those on extremely controversial topics.

- Fact-Checking 9/11, the JFK Assassination, the Covid Outbreak, the Holocaust, and Other Controversial Topics

- Ron Unz • The Unz Review • June 9, 2025 • 7,400 Words

- Fact-Checking the Jeffrey Epstein Case and Many Other Conspiracy Theories

- Ron Unz • The Unz Review • July 14, 2025 • 8,100 Words

- Fact-Checking the Remarkable Revelations of Three Dozen Unknown Books

- Ron Unz • The Unz Review • November 24, 2025 • 9,500 Words

I've actually been a little surprised that no other websites I've encountered appear to have integrated AI systems into their content in these sorts of ways.

A Gigantic Bubble in AI Tech Stocks?Those Deep Research fact-checking runs averaged well over 10,000 words each. Given the enormous time and computer resources they must have required, I felt sure that the $200 monthly fee covered just a sliver of their real cost, even joking that OpenAI was probably subsidizing those prices by 99% or more. Therefore, I urgently worked to finish all the runs on my many hundreds of old articles before the company raised the price to something closer to its true expenses or else went bankrupt.

Although OpenAI has continued to raise billions or even tens of billions of dollars in venture capital at rapidly increasing valuations, I think my concerns proved fully justified.

Just a couple of months ago, OpenAI pulled the plug on its very high profile Sora video platform project despite the agreement the company had already inked with Disney for a $1 billion investment. Apparently that decision was made because the company needed to conserve its resources and focus them on its core operations in preparation for its intended IPO later this year.

Around the same time, the quality of the Deep Research runs dropped so dramatically that they became almost useless, so I stopped bothering to produce them for my subsequent articles. Apparently OpenAI had lobotomized its Deep Research system for much the same reason. The quality of the responses produced by the customized author Chatbots also very sharply declined.

As I've emphasized, I found these AI technologies extremely impressive to use but I was never convinced that they were cost-effective enough to survive in the marketplace. The answer to this question obviously has enormous consequences for the health of our overall economy.

Our AI boom of the last few years has been of absolutely unprecedented magnitude, dwarfing the notorious Internet investment frenzy of the late 1990s Dotcom era.

Subscribe to New Columns

The total market value of all these public and private companies is probably in the vicinity of $30 trillion or more, about the same size as the entire American economy. Indeed, AI-related investment was responsible for roughly half of all American GDP growth during the most recent quarter.

From its inception, OpenAI has been the high-profile public face of the AI revolution, and it has now raised $180 billion in venture capital across 15 separate funding rounds, reaching a current valuation of $852 billion despite never turning a profit.

And right around the time of that dramatic announcement of a new record-breaking investment of $122 billion, the OpenAI Deep Research system stopped working properly, which raised all sorts of questions in my mind.

I'd gradually become aware of an especially fierce critic of the AI industry named Ed Zitron, and I'd read one of his many recent posts on the subject.

For the last few years, Zitron has been ferociously denouncing the financial structure of the entire AI sector as merely a fragile house of cards, a gigantic bubble that was very likely to soon collapse and take down some enormous corporations along with it.

In that particular lengthy posting, written in his characteristically pungent style, Zitron argued that the AI industry shared some characteristics with a Ponzi scheme, claiming that large new injections of investment venture capital were effectively being converted into the circular revenue streams that have so impressed many of those supplying that funding.

- Am I Meant To Be Impressed?

- AI Revenues Are Pathetic and Circular, With OpenAI Representing 71%+ Of Microsoft's AI Run Rate and Anthropic 80% of Amazon's

- Ed Zitron • Substack • May 6, 2026 • 9,800 Words

I also discovered that last October I'd previously cited a brief excerpt from one of his previous posts quoted on the Naked Capitalism blog.

Where we sit today is a time of immense tension. Mark Zuckerberg says we're in a bubble, Sam Altman says we're in a bubble, Alibaba Chairman and billionaire Joe Tsai says we're in a bubble , Apollo says we're in a bubble, nobody is making money and nobody knows why they're actually doing this anymore, just that they must do it immediately.

And they have yet to make the case that generative AI warranted any of these expenditures.

Zitron is an extremely prolific blogger who has published posts totaling many hundreds of thousands of words over the last year or so, all them denouncing the financial structure of the AI industry, and doing so with a great deal of detail and tremendous exuberance.

Over the last week or two, his analysis attracted my interest. So as a total newcomer to these issues, I sat down and read a dozen or so of his long posts, generally finding them extremely informative and fairly persuasive.

The two main AI companies are OpenAI and Anthropic, the latter of which was founded in 2021 mostly by a group of former OpenAI employees. Although OpenAI had long been the face of the technology, Anthropic may have recently edged into the lead, with its latest funding round now valuing it at $965 billion. Both companies were hoping for IPOs some time this year.

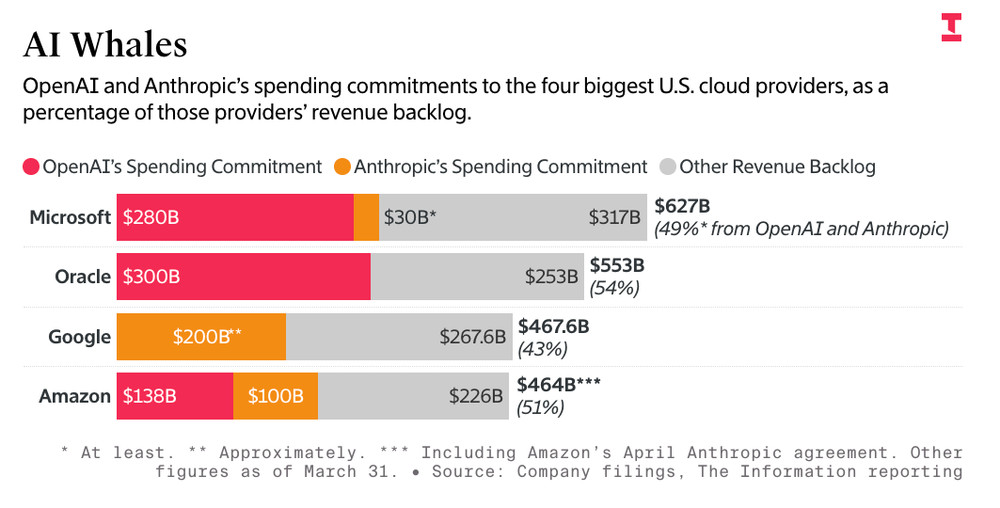

One of Zitron's main arguments is that neither OpenAI nor Anthropic have any plausible path to profitability. Despite this they have made enormous contractual commitments to Microsoft, Google, Amazon, and Oracle, most of which are simultaneously providing them the investment capital that keeps them alive. As he wrote in early May:

The Information's story also had this fascinating chart showing that around 50% of Amazon, Google and Microsoft's backlog (which includes all revenues not just AI) — a staggering amount — is made up of revenue from OpenAI and Anthropic:

Just two weeks ago, both Amazon and Google pledged to invest up to another combined $65 billion in Anthropic, a company that just raised $30 billion in February and plans to raise another $50 billion more, following Amazon's $15 billion (and as much as $35 billion more) investment in OpenAI in February.

This is not what you do when real, meaningful demand exists for AI services. Assuming that these rounds are closed at their higher limits, it will mean that Google has invested $43 billion and Amazon $33 billion in keeping Anthropic alive.

As I've explained, most AI revenues out of Google, Microsoft and Amazon come from two companies that lose billions of dollars a year, have no path to profitability, and are only able to keep paying these companies because the companies (and investors) keep feeding them money.

These relationships are utterly poisonous, and an intentional attempt to deceive investors and the general public.

So the Tech giants have invested enormous sums in OpenAI and Anthropic which then return those same dollars in the form of payments for services. Similarly, the bulk of the payments to Anthropic and OpenAI comes from other money-losing AI startups, whose venture capital investments become revenue for those larger companies. Much of this reminds me of the last stages of the Dotcom bubble.

Just a couple of days of reading though his posts hardly give me the expertise to evaluate them, but I think that if even 10% of his claims turn out to be correct, the entire AI industry seems doomed to collapse.

He was skeptical about the likelihood of a successful IPO for either OpenAI or Anthropic, so if those companies did survive, they would probably be acquired at fire sale prices by Microsoft, Google, or Amazon. Meanwhile, Oracle has staked its entire future on OpenAI, so Oracle's survival is very much in question.

One of Zitron's most remarkable claims was that a substantial fraction of the ultra-expensive AI chips supposedly sold and shipped by Nvidia over the last year or two may have never actually left Taiwan. He argues that AI data center construction is often so far behind schedule that the chips and the racks housing them have probably remained in Taiwanese warehouses gathering dust, perhaps likely to already have become obsolescent by the time they are finally installed and activated.

Given the enormous volume of his material and my own ignorance of this complex topic, I'd simply urge those interested to read a couple of his lengthy posts and decide for themselves. I'm providing a convenient listing of the major posts from the last twelve months. Most of the titles are quite descriptive, and those marked with a "[P]" contain some material that is only available to paid subscribers.

P What If...We're In An AI Bubble ? (Part 3) • May 29, 2026 • 15,700 W

Revenge of The Business Idiot • May 26, 2026 • 10,600 W

P What If...We're In An AI Bubble ? (Part 2) • May 22, 2026 • 8,600 W

Anthropic's "Profitability" Swindle • May 21, 2026 • 2,200 W

AI Is Too Expensive • May 19, 2026 • 8,600 W

P What If...We're In An AI Bubble ? (Part 1) • May 15, 2026 • 11,700 W

Where Are All The Data Centers? • May 12, 2026 • 9,600 W

P AI's Circular Psychosis • May 8, 2026 • 8,500 W

Am I Meant To Be Impressed? • May 6, 2026 • 9,800 W

P The AI Compute Demand Story Is A Lie • May 4, 2026 • 8,300 W

AI's Economics Don't Make Sense • April 28, 2026 • 9,400 W

P How OpenAI Kills Oracle • April 24, 2026 • 9,600 W

Four Horsemen of the AIpocalypse • April 21, 2026 • 5,600 W

P The Hater's Guide to Private Credit • April 17, 2026 • 15,700 W

I Will Never Respect A Website • April 14, 2026 • 11,000 W

P The Hater's Guide to OpenAI • April 10, 2026 • 16,900 W

AI Is Really Weird • April 8, 2026 • 10,800 W

P AI Isn't Too Big To Fail • April 3, 2026 • 18,200 W

The Subprime AI Crisis Is Here • March 31, 2026 • 10,700 W

P How Much Of The AI Bubble Is Real? • March 27, 2026 • 13,600 W

The AI Industry Is Lying To You • March 24, 2026 • 9,400 W

P The Hater's Guide To The SaaSpocalypse • March 13, 2026 • 12,600 W

The Beginning Of History • March 10, 2026 • 6,500 W

P The Hater's Guide to Private Equity • February 27, 2026 • 16,500 W

P The Hater's Guide to Anthropic • February 20, 2026 • 16,400 W

P The AI Data Center Financial Crisis • February 13, 2026 • 14,800 W

P The Hater's Guide to Oracle • January 30, 2026 • 16,200 W

P This Is Worse Than The Dot Com Bubble • January 16, 2026 • 13,600 W

The Enshittifinancial Crisis • December 29, 2025 • 18,700 W

NVIDIA Isn't Enron - So What Is It? • December 8, 2025 • 14,600 W

P The Hater's Guide To NVIDIA • November 24, 2025 • 14,000 W

Big Tech Needs $2 Trillion In AI Revenue By 2030 or They Wasted Their Capex • October 31, 2025 • 10,200 W

The Case Against Generative AI • September 29, 2025 • 18,700 W

Is There Any Real Money In Renting Out AI GPUs? • September 19, 2025 • 6,800 W

Oracle and OpenAI Are Full Of Crap • September 12, 2025 • 7,700 W

Why Everybody Is Losing Money On AI • September 5, 2025 • 8,400 W

How To Argue With An AI Booster • August 25, 2025 • 15,800 W

Anthropic and OpenAI Have Begun The Subprime AI Crisis • July 7, 2025 • 9,500 W